Click here to download a PDF of this article

Introduction

Collectively as GHG professionals, we are confused about what an “emission reduction” is. This confusion is interwoven within several of the long-running debates within the climate change community. At the root of this confusion is a widespread failure to explicitly communicate what we mean when we say “reduction”—we all too frequently fail to communicate what the reduction is relative to? If we could eliminate this confusion, we could considerably elevate the quality of our communication and more effectively resolve debates.

Types of GHG accounting

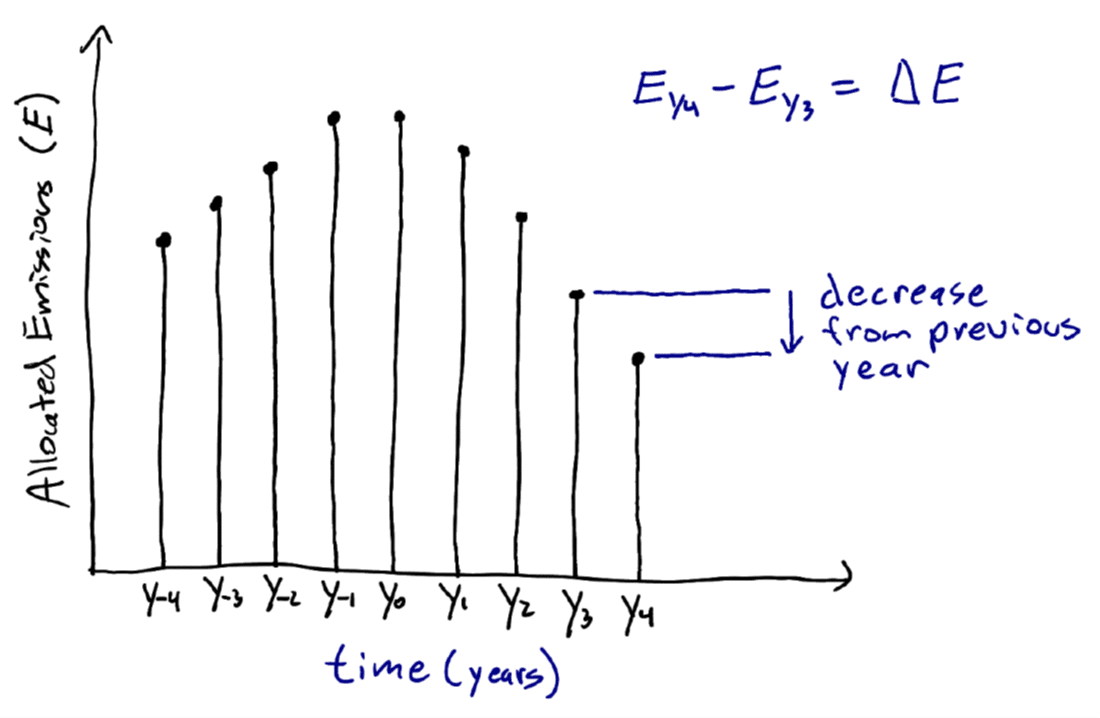

Avoiding confusion requires distinguishing between two different points of reference against which “reductions” are assessed. You should be familiar with these relative references, as they correspond to the two types of physical GHG accounting—allocational and consequential. The first relative reference is simply a prior point in time when an allocational (i.e., inventory) method was applied. For example, we total emissions allocated to a company each year in a time series and then refer to a decrease between two successive years’ totals as an emission reduction (Figure 1).

Figure 1. Illustration of an emission reduction (ΔE) in year 4 (Ey4) relative to year 3 (Ey3) within a GHG inventory[1]

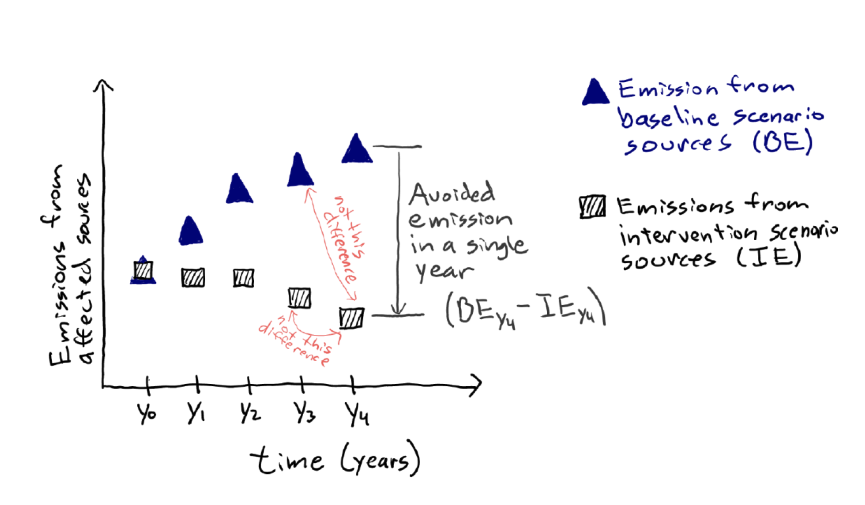

The second relative reference is an alternative scenario for emissions within the same year (i.e., the identical period of time) applied when using a consequential accounting method. The alternative scenario is one in which an intervention (e.g., an action, carbon crediting project, policy change), and its resulting causal impacts, do not occur. Generally, we refer to the scenario without the intervention as the baseline scenario and the scenario with the intervention as the intervention, project, or policy scenario (Figure 2).

Figure 2. Illustration of temporal aspects of avoided emissions when using a consequential GHG accounting method

These two types of references, derived from allocational and consequential GHG accounting analysis, respectively, are so commonly used that they may seem banal. Yet, it is almost a universal practice to refer to both types of relative changes in emissions as “emission reductions” without any explicit clarification of what the reduction is relative to. At worst, it is common for many to act as if they are the same thing. Yet, the fundamental calculation of each type of change applies both a fundamentally different temporal reference as well as a different conceptual basis for setting the GHG accounting boundary.

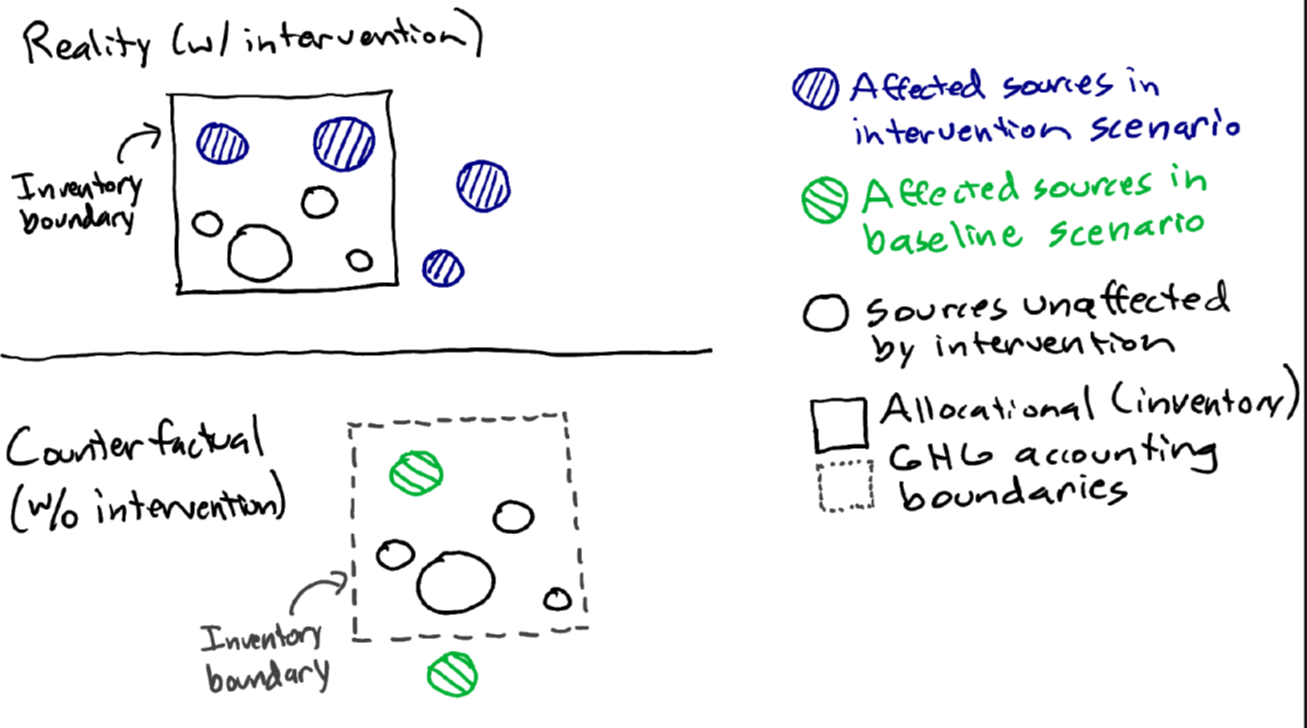

As explained here, the accounting boundaries for allocational accounting include all emission sources and removal sinks an entity is assigned responsibility for in a consistent manner over time. While the accounting boundaries for consequential accounting include only those emission sources and removal sinks that are altered by the considered intervention (i.e., sources and sinks that differ between the intervention and baseline scenarios). These differences in allocational and consequential GHG accounting boundaries are illustrated in Figure 3.

Figure 3. Illustration of boundary setting distinctions between allocational (inventory) and consequential (intervention) GHG accounting

It’s past time to elevate our nomenclature

The problem is that our common practice nomenclature has been failing us. Even when we understand the difference, we have been stuck using the same phrase—”emission reduction”—for two different measures of change. This linguistic ambiguity would not matter if it was not muddling, and thereby slowing progress on, numerous key climate action debates such as the proper role of offsetting claims through credits, market-based GHG accounting approaches, and Scope 3 emission estimates. We have become so used to the ambiguity that we often do not even notice it. The time is well passed for all of us all to speak with more clarity.

The origin of this nomenclature error can be found in the early days of environmental offsetting.[2] Offsetting entails the substitution of a reduction over time in an entity’s pollutant inventory with changes caused elsewhere by an intervention estimated with a consequential method. Because policy makers have treated these changes as being equivalent for judging regulatory compliance for facilities under a collective cap on their emissions, we all fell into the habit of calling them both “emission reductions” and failed to develop a habit or language distinguishing them though the two types of changes entail different temporal and boundary setting references. More intuitively, decades of controversy over offsetting claims should have also taught us that claims regarding the two types of changes in a voluntary corporate claims context are not perceived to be conceptually, technically, or morally equivalent.

What we need is two separate terms—one for a decrease in inventoried emissions over time and another term for the decrease in emissions caused by an intervention at the same point in time. This will eliminate the ambiguity and confusion in our debates and writing. At the GHG Management Institute, we have already begun using the following nomenclature in our communications and teaching to clearly distinguish the type of decrease and GHG accounting we are referring to (Table 1).

Table 1. Type of Physical GHG Accounting

| Quantification nomenclature | Positive and negative change nomenclature | |

|---|---|---|

| Allocational (Inventory) | Emissions from sources | Emission reductions |

Removals by sinks | Increase in removals |

|

| Consequential (Intervention) | Avoided emissions |

|

Enhanced removals |

||

| * More commonly used terms are underlined | ||

Application of the nomenclature in Table 1 limits the use of the term “emission reduction” to only refer to decreases in emissions over time. In contrast, the intended impact of interventions in all cases is to avoid emissions that would otherwise have been emitted if not for an intervention or enhance the quantity of removals that would not have been removed if not for an intervention. The purpose of having separate terms is to distinctly convey, with one word (i.e., “reduced” versus “avoided”), the applicable type of physical GHG accounting and the what the change being referred to is fundamentally in reference to.

Two significant implications of this improved nomenclature are that quantified consequential intervention impact claims, such as those in the carbon credit markets, should use the term “avoided emissions” and cease referring to their claims as emission reductions.[3] Crediting market actors should also cease referring to their claims as “removals,” which is a well-established GHG inventory term, and instead consistently use the term “enhanced removals” for all crediting impact claims, including those in which the baseline scenario level of removals is zero.

Why is avoided the right term?

Some crediting market actors have proposed a range of terms to distinguish between different types of projects, for example, labeling projects as resulting in emission reductions, avoided emissions, or emissions destruction. These actors would define projects that install abatement equipment at nitric acid plants as “reducing” N2O emissions from nitric acid production; projects that prevent deforestation are said to “avoid” emissions that would have occurred from deforestation; and methane capture projects are defined as “destroying” methane (CH4) through combustion. From a GHG accounting perspective, however, these distinctions are arbitrary. For example, the nitric acid plant case could just as easily be referred to as destruction, deforestation prevention could be conceptualized as a reduction of forest harvest-related emissions, and methane capture could be termed as an avoidance project as the combustion avoids the emissions of methane into the atmosphere. These distinctions are neither objective nor helpful in understanding the underlying GHG accounting method and are a poor substitute for communicating the type of process changes involved in these interventions or what the changes are measured relative to. Instead, it should be clear that in all these cases, the outcome is that an intervention is claimed to have avoided the release of GHG emissions into the atmosphere that would have occurred under the baseline scenario (i.e., without the intervention).[4] This fact is not altered by the type of technology used to achieve this avoidance of emissions.

Predictably, actors in carbon credit markets may struggle with this linguistic shift. Change is sometimes hard. We now have decades of legacy documents that have used “emission reduction” to refer to everything. Plus, there is still a bias in the carbon credit markets to maintain the illusion of an unqualified equivalence between the two types of changes in emissions. It is important to recognize that an emission reduction in inventoried emissions over time is not inherently superior to or more accurately estimated than estimates of avoided emissions due to an intervention. Similarly, enhanced removals due to an intervention are not inherently superior to or more accurately estimated than changes in inventoried removals from sinks over time.[5] The two approaches to conceptualizing and quantifying changes are different even though it is offsetting claims, through the use of carbon credits, have tended to come under more scrutiny for environmental integrity issues.

Lastly, when your communications require further precision, you should endeavor to specify what exactly the changes you are communicating about are relative to. For example, emission reductions in company Alpha’s GHG inventory in 2025 relative to its emissions in 2010. Or the Beta coal mine project’s avoided emissions in the year 2024 relative to the without-project (or baseline) scenario.[6]

So what do we do?

Now is the time to make this shift in terminology given that the GHG Protocol is being revised, regulatory programs around the world are increasingly considering GHG accounting requirements, and the voluntary carbon credit market is being deeply scrutinized and responding with significant revisions to methodologies.

Do you care about solving the profound problems within the current practice of corporate GHG accounting and reporting? If so, I encourage you to join in this effort by using the nomenclature identified in Table 1. Push back against the lazy habit of being ambiguous and push back against those who argue we have to keep doing things like we always have. If they work in the carbon credit market, just ask them to think about how well that has been working recently? Or more strategically, ask them to consider if increasing clarity and understanding of carbon credits will help their cause? Wouldn’t an improvement in the clarity of terminology at least aid in rebuilding trust in the environmental integrity of carbon credits?

Click here to download a PDF of this article

Acknowledgments

I am thankful for the insightful comments from my colleagues Derik Broekhoff (SEI) and Tani Colbert-Sangree (GHGMI).

Recommended Citation

Gillenwater, M., (2023). “What is an “emission reduction”? And when you should be you avoiding saying “reduced”?”. Seattle, WA. Greenhouse Gas Management Institute, January 2025. https://ghginstitute.org/2025/01/21/what-is-an-emission-reduction-and-when-should-you-avoid-saying-reduced/

[1] To be precise, the emissions labeled as y1 are the aggregate emissions occurring over the period to time from the end of y0 to the end of y1 (i.e., end of yn-1 to end of yn) [2] See Gillenwater (2011), “What is Additionality? Part 1: A long-standing problem” for a discussion of the history of offsetting. [3] Some organizations have been unhelpfully trying to define the term “avoided emissions” as only being related to estimating the differences in product life-cycle emissions that result from changes to products. It is not clear why we need a separate term for changes specifically for product level environmental accounting, especially given the long-running failure that the product life-cycle assessment community has exhibited in distinguishing between results using allocational and consequential methods (see here). [4] Some actors even maintain that reduction or removal activities are more credible as offsets than activities that “avoid” emissions – since “avoidance” often means the continuation of the prior activity or behavior. This is not inherently true; what matters for credibility is how certain the baseline is and whether the activity is additional. [5] Although, one could argue that changes in emissions over time in a global GHG inventory are inherently superior to a consequential estimate as the former is near-perfectly correlated with the ultimate objective measure of progress, which is atmospheric GHG concentrations. [6] If you are wondering about how the assessment of additionality relates to such statements, see here.

Image: Robbie Andrews (2019); based on Global Carbon Project & IPPC SR15, CC BY

Comments