What is GHG Accounting? Market-based approaches in multi-statement GHG reporting (Installment N.7 bis)

Executive Summary

Corporate greenhouse gas (GHG) accounting is facing a credibility challenge. Current practices allow companies to use market-based instruments like renewable energy certificates (RECs) to modify their reported emissions, often without a clear link to actual emission reductions. This has led to widespread confusion, accusations of greenwashing, and growing skepticism about the integrity of corporate climate claims.

This paper, and its companion Installment N.7, proposes a solution—a multi-statement corporate GHG accounting framework that separates the measurement of physical emissions from the recognition of mitigation impact. The core idea is that no single emissions number can serve all the purposes of GHG reporting. Instead, distinct reporting statements should serve distinct functions:

Physical Inventory: Reports actual emissions using activity-based data and average emission factors from shared systems, referred to as activity pools (such as electricity grids). This reflects the physical emissions that a company is to take responsibility for.

Mitigation Intervention: Reports avoided emissions resulting from voluntary corporate actions, such as clean energy investments or participation in environmental attribute certificate markets. These impacts are calculated using consequential methods that assess whether, and how much, emissions were avoided or removals enhanced compared to a credible no-intervention baseline scenario.

Market-based instruments should not be used to overwrite physical emissions in inventories. Their real value lies in their ability to incentivize mitigation through financial and contractual commitments. Treating them as such, and reporting their impact separately, restores integrity to emissions accounting while recognizing companies for their contributions to broader decarbonization.

By adopting this framework, corporate climate reporting becomes more transparent, defensible, and aligned with real-world outcomes. It also enables companies to pursue high-impact interventions without distorting their emissions inventories, ultimately leading to more effective climate action.

Introduction

Imagine a future in which companies were simultaneously recognized for indirect emission reductions due to their electrical energy efficiency improvements and for the actual avoided emission impacts of their interventions into renewable energy power markets. In this future, the claims made by companies based on the resources they spend on Environmental Attribute Certificates (EACs) and other market-based instruments are broadly recognized as valid because they are appropriately accounted for based on their positive impact, avoiding greenhouse gas (GHG) emissions and enhancing carbon removals. For example, for Scope 2, this means shifting corporate GHG accounting from a focus on MWh matching claims to measures of physical GHG impacts. Imagine that the intense debates and greenwashing criticisms over how to account for Renewable Energy Certificates (RECs), Power Purchase Agreements (PPAs), and other EACs are finally settled. Such a vision should not be a fantasy; it should be our expectation so that voluntary corporate action can be fully unleashed and appropriately recognized. But to get there, we will need to rethink the role of market-based claims and instruments in corporate GHG accounting, letting go of outdated assumptions.

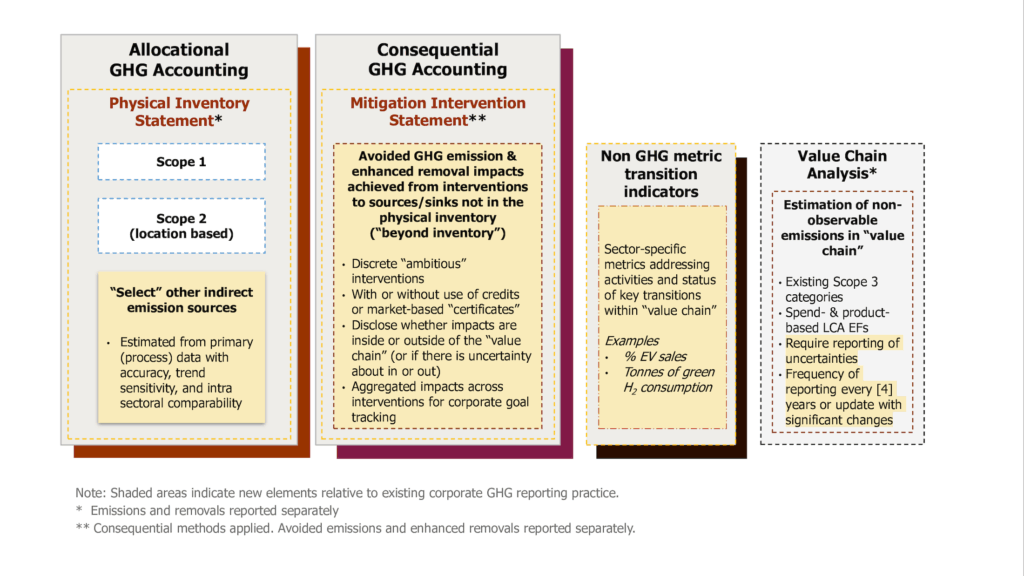

This installment elaborates on “Paradigm shift to multi-statement GHG reporting” (Installment N.7), which introduced an improved framework for corporate GHG accounting that solves fundamental problems with the existing value chain GHG inventory paradigm (Figure 1). Specifically, this installment focuses on the elements of this paradigm shift related to market-based approaches to Scope 2 and GHG accounting more broadly. The justification for a shift to multiple reporting statements is that no single metric, such as a corporate GHG inventory, can meaningfully serve all intended uses of corporate GHG information. We need multiple metrics to support multiple intended uses for corporate GHG data.

Figure 1. Illustration of proposed multi-statement corporate GHG reporting1

Why use a market-based approach?

Why would we include market-based approaches in any form of corporate GHG reporting? Like with emissions trading mechanisms, doing so entails introducing significant governance burdens as well as other administrative and transaction costs—to issue, transact, police the environmental commodity market, prevent double counting, and especially ensure the environmental integrity of EACs and other instruments. When inserted into corporate GHG inventory protocols, they effectively allow companies to purchase an emission factor that is either unconnected to or not exclusively representative of their physical activities (e.g., RECs that are not representative of all the physical sources of electricity consumed by a company). Market-based inventory approaches do not improve the technical accuracy of physical GHG inventory accounting. They instead substitute physical inventory estimates with claims based on purely financial transactions for claimed energy and/or environmental attributes. But there are reasons to use market-based approaches because they can be powerful policy tools to achieve mitigation.

The only reason for including market-based approaches in any form of corporate GHG reporting is that we expect the aggregate of all market-based instrument transactions to result in additional mitigation action (i.e., will cause global atmospheric emissions to be avoided and removals enhanced compared to a world in which the market-based approach was not included in a GHG accounting protocol). If we do not have confidence that a market-based approach will produce such a beneficial aggregate mitigation outcome, then it is a waste of resources, and we should not allow it under corporate GHG reporting standards. Because if we do, then we must understand that it will eventually be exposed as greenwashing and damage the credibility and, therefore, perceived value of corporate recognition labels.2

There is no point in establishing and policing market-based instruments and other contractual claims if, in the end, they are just shuffling the allocation of reported emissions between reporting entities and non-reporting entities. For example, if a company reports the retirement of RECs, and thereby claims a zero Scope 2 emission factor in its corporate GHG inventory, the implication is that indirect emissions are being reallocated from fossil-fuel fired generation associated with the company’s actual physical consumption of electricity to other consumers receiving grid-supplied electricity—regardless of whether these other consumers are tracking and reporting the indirect emissions from their electricity consumption. We must remember that corporate GHG reporting typically occurs in the context of voluntary, or limited mandatory, reporting, where many companies do not participate, and in which science-aligned corporate reduction target setting is not common practice.

Put simply, market-based methods have been incorrectly classified as suitable for allocational (inventory) GHG accounting. Correctly, we must understand market-based approaches to corporate GHG reporting as being an environmental market mechanism for the intended purpose of achieving a policy objective. They are inherently NOT policy neutral and have many market design needs that go well beyond GHG inventory methodologies.3 Physical GHG inventories quantify emissions and removals over time occurring within clearly defined accounting boundaries. Nothing more. Both serve different but complementary roles. Mixing them, as the Scope 2 market-based method within the GHG Protocol does, compromises the integrity of both emission measurement and mitigation policy efficacy.

The Scope 2 dead-end path

Market-based approaches in corporate GHG accounting originated with the use of RECs in Scope 2 reporting. From the beginning, the practice has been debated and frequently criticized for fostering greenwashing by allowing companies to misleadingly report that the generation of electricity they consume does not emit any GHGs. Despite these critiques and an emerging empirical evidence of a lack of efficacy, the practice was later endorsed by the GHG Protocol in 2015 despite objections from members of its technical working group. Eventually, the expanding evidence base showing a lack of efficacy of the voluntary REC market4 led companies to seek alternatives viewed as more impactful, such as virtual PPAs and, more recently, 24/7 matching with hourly RECs.5 Without a well-recognized complementary GHG reporting framework for consequentially quantified avoided emission impacts, companies have been constrained by having to report all these market-based actions under Scope 2 as MWh matching claims without differentiation as to their GHG mitigation efficacy. In other words, when market-based approaches are used for reporting Scope 2, and more recently Scopes 1 and 3, they allow companies to buy from “emission attribute” markets with unevaluated and sometimes no mitigation efficacy.

The current belief is that actions taken by companies via EACs and other market-based instruments only count if they are reflected in the intervening company’s GHG inventory and counted toward their inventory reduction target. Conversely, a high-impact action taken by a company that does not fall within its deemed inventory (e.g., helping to bring online a new solar farm in a high-emissions intensity grid but which is located outside of its operational boundary) falls outside that company’s inventory reduction target. As a result, sellers and marketers in the rapidly growing marketplace for EACs feel compelled to advertise their certificates as appropriate for matching and thereby overwriting a company’s physical consumption and physical emissions. For example, RECs and PPAs are sold with claims that they can be used to replace a company’s location-based Scope 2 emissions in target setting. More recently, biogas attribute certificates and Sustainable Aviation Fuel (SAF) attribute certificates have been sold with claims that a company can overwrite physically occurring Scope 1 and/or Scope 3 emissions. When these market-based approaches are used in GHG inventories, they effectively introduce a form of emissions trading that allows companies to offload “their” emissions without other companies taking responsibility for the transferred emissions due to the voluntary character of corporate GHG reporting.

Again, the actual function of market-based approaches is to channel and aggregate mitigation interventions (e.g., induce additional investment in solar energy capacity or SAF utilization) through organized environmental markets. The use of market-based instruments is unnecessary to mitigate emission sources that a company already has considerable control over (i.e., sources within its physical GHG inventory). And there are several vexing methodological problems created by the introduction of market-based approaches to GHG inventory accounting for direct and indirect emissions (i.e., Scopes 1, 2, and 3) that a Mitigation Intervention statement largely escapes (see Annex A).

However, market-based approaches are appropriate to address sources a company does not have clear visibility of or considerable physical control over (i.e., sources beyond a company’s physical inventory boundaries and in activity pools, see Box 1). The avoided emissions impact of these market-scale interventions can be reported in a separate GHG accounting statement—a Mitigation Intervention statement.

Box 1. What is an activity pool?

In the context of allocational or GHG inventory accounting, an activity pool is defined as a common set of emission sources with processes that physically serve (i.e., are connected via matter or energy flows) an accounting subject (e.g., company), in cases where traceability from the specific physical source of emissions to a specific accounting subject is not possible (Brander and Bjørn, 2023; Gillenwater, 2023). The most well-known activity pool is a shared electricity distribution grid, along with the generators connected to it. But other examples include natural gas pipeline networks, agricultural and raw material commodities, and waste management systems used for the disposal of sold products. Because consumption or production of products or services by companies from an activity pool is from a mixture that cannot be differentiated with respect to its upstream or downstream processing, emissions are logically allocated based on the average emissions intensity (i.e., emission factor) of that pool. Any other allocation rule would presume exclusive physical traceability exists, when in truth it does not, or would allow emissions to be reallocated between companies based on purely financial or contractual arrangements.

Quantifying market-based impacts in a Mitigation Intervention statement

The Mitigation Intervention statement resolves the deeply rooted disconnect between corporate actions and recognition that plagues the existing GHG Protocol corporate standard’s approach to indirect emissions (i.e., Scopes 2 and 3). It creates a dedicated reporting and goal-setting metric that recognizes ambitious contributions via EACs and other market-based instruments to global mitigation. Separating the accounting of “beyond inventory” and activity pool intervention impacts from physical inventory accounting eliminates the many problems created by the “financialization” of policy-neutral corporate GHG inventory accounting (i.e., allowing companies to purchase substitute emission factors) because it correctly treats market-based approaches as market mechanisms that recognize, and thereby incentivize, interventions in proportion to their GHG impact.

The Mitigation Intervention statement evaluates the avoided emission impacts of EAC-based interventions at the scale of the overall EAC market. In other words, the impacts of organized environmental commodity markets are first quantified in aggregate as a market-scale intervention because that is what they are—and because it is impractical to assume the impact of each corporate transaction of EACs can be individually quantified.6 These aggregate impact estimates of the overall EAC market for each year are then assigned to companies based on the share of EACs of that year’s vintage they hold. For example, the avoided emissions impact of the entire SAF certificate market would be estimated each year and then claimed and reported proportionally by each certificate holder of that year’s certificate vintage. Similarly, for hourly REC holders, the analysis of the impacts of the hourly REC market each year would be estimated and then apportioned across hourly vintages and holders of those vintages, which then would report and claim their share of these impacts in their Mitigation Intervention reporting and count them toward their contribution goals7.

However, not all corporate interventions are taken through EACs. Some are taken through a company’s direct physical or financial actions. For example, the GHG-related purpose of a corporate PPA (see Box 2) is to make a financial subsidization and risk-transfer intervention within renewable energy markets for the purpose of causing additional renewable energy deployment and thereby displacing GHG emissions from fossil fuel-fired generation. As a form of intervention, corporate PPAs act more through their risk transfer effect (i.e., shifting some financial risk from renewable energy developers to corporate offtakers; see Box 3). They make it easier for project developers to raise investment capital and lower the cost of that capital, thereby potentially causing the development of additional renewable energy generation capacity.

Given that corporate PPAs vary significantly in their displacement impact on GHG emissions from the electric power sector activity pool, they should be accounted for based on how much fossil fuel combustion is displaced by the PPA compared to an alternative in which the PPA was not executed. Methodologies for quantifying PPAs’ avoided emission impacts need to address the variation in wholesale power market and regulatory contexts and contract terms, which determine how risk is transferred. Instead, the current Scope 2 market-based approach—that relies on MWh matching—allows companies to “zero-out” their inventoried indirect emissions associated with their physical consumption of electricity, regardless of how much or whether the PPA displaces power sector emissions. Because of this misdirected focus on MWh matching—regardless of the granularity, annual or hourly—we do not yet have well-established methodologies for quantifying the impact of PPAs and many other types of corporate financial interventions.8 In a future installment, we will outline a proposed research agenda with a practical path to developing an evidence-based corporate renewable energy PPA consequential methodology—one that addresses both the quantification of displaced emissions and criteria for evaluating which PPAs have been sufficiently determinative in causing capacity additions.

Box 2. What is a Power Purchase Agreement?

There are different kinds of Power Purchase Agreements (PPAs). Physical PPAs have long been used by load-serving entities (LSEs) (e.g., utility companies that sell and distribute power to retail consumers) to contract with generators and thereby fulfill electricity load delivery obligations to electricity consumers. They’re also sometimes used by non-utility companies, often in coordination with their LSE. In either case, the buyer pays an electricity generator, according to a long-term pricing structure, typically for supplying a specified or floating amount of power that’s injected at designated transmission grid nodes and times. In contrast, Virtual PPAs are multi-year contracts that allow end-use companies (e.g., non-utilities) to engage in financial hedging on wholesale electricity prices directly with generators without altering physical power deliveries for LSEs in wholesale or retail power markets. In both types of PPA, the buyer assumes the energy price risk associated with the project, making it a more attractive investment, which will ideally enable its construction. In exchange, the buyer hopes to receive long-term electricity pricing benefits and a stream of RECs initially issued to the renewable energy generator. Both types of PPAs have the potential to function as an effective mitigation intervention.

Box 3. Corporate offtakers in virtual PPAs

An “offtaker” in a virtual Power Purchase Agreement (vPPA) is the counterparty that contractually agrees to purchase Renewable Energy Certificates (RECs) from a renewable energy project and assumes some or all of the financial exposure to electricity price volatility from a renewable energy project, without taking physical delivery of the electricity (see Box 2).

Typically, a corporate offtaker enters into a “contract for differences” in which:

The offtaker pays the renewable energy generator a fixed strike price for each MWh of electricity generated, while simultaneously receiving payments equal to the prevailing wholesale power market electricity price (typically the locational marginal price) for that same generation.

When the wholesale price is less than the strike price, the offtaker pays the generator the strike price minus the wholesale price. When the wholesale price is more than the strike price, the generator pays the offtaker the wholesale price minus the strike price.

And the offtaker receives the RECs issued to the generator for the portion of generation under contract.

Unless they are an electric transmission or distribution company engaged through a physical PPA, a corporate offtaker does not physically receive the electricity generated, which instead is injected into the wholesale transmission grid for distribution to and use by all consumers connected to that grid. The offtaker’s physical load is served by their local distribution utility through standard retail arrangements. vPPAs create a purely financial relationship with an electricity generator. But through that financial relationship, corporate offtakers typically provide credit enhancements (i.e., financial guarantees, letters of credit, or cash collateral) to secure their payment obligations under the long-term contract structure. Financing a new renewable energy project without this type of offtake contract is extremely difficult in most power markets. The offtaker’s commitment, thereby, removes some financial risk from the project developer by providing greater long-term revenue certainty necessary to access upfront project financing.

What about induced emissions?

The primary purpose of the Mitigation Intervention statement is to report the impact of corporate interventions that are intended to avoid emissions and enhance removals relative to the scenario in which they did not intervene. Many actions taken by companies, however, can also induce emissions and inhibit removals. How might these detrimental actions be reported? As discussed above, any market-based mechanism that, in aggregate, induces—rather than avoids emissions—should not be allowed under GHG accounting rules. Why would we create an EAC or other market-based contractual instrument and marketplace that, in aggregate, makes climate change worse?

Under the current GHG Protocol Scope 2 Technical Working Group process to update guidance on Scope 2, a different and new type of “all consumption” induced emissions metric has been proposed. It is estimated based on the application of marginal emission factors (i.e., addressing both operating short-term and long-term, or build, marginal emissions) for grid-connected electricity generation. By applying these factors to a company’s total electricity consumption, it is possible to estimate an induced emissions metric that approximates the marginal increase in electric sector emissions attributable to the company’s consumption. A simplistic interpretation of such an analysis is that it quantifies how much emissions from electricity generation were caused by the company’s existence and operations in the economy.9 However, a proper consequential analysis of that question accounts for the fact that if a company completely ceased consuming electricity and ceased production (i.e., shut down its business), the demand for its services would largely be shifted to other companies, which would then increase their electricity consumption. Yet, if examined at a disaggregated activity or process level, an induced emissions metric does indicate where and when energy efficiency improvements (i.e., reduced consumption) would have the largest avoided emissions impact.

Although both avoided emissions reported under the Mitigation Intervention statement and this new “all consumption” induced emissions estimate are produced using consequential methods, they use fundamentally different baseline scenario assumptions.10 So, a net sum of these two metrics is not a correct physical GHG accounting measure; however, some form of combined net score could be created as a Performance GHG accounting scorecard. An “all consumption” induced emissions metric could serve as a reference for setting the size of a company’s contribution goal for its Mitigation Intervention statement (see Installment N.7).

How do market-based approaches fit into a multi-statement framework?

In parallel with the discussion in Installment N.7, below is a summarized explanation of the role of market-based approaches and claims within each statement in the proposed multi-statement GHG reporting framework illustrated in Figure 1.

The Physical Inventory statement, which relies on a location-based method for Scope 2, includes no role for EACs and other market-based accounting approaches and claims. Sources and sinks reported under this statement must be physically identified with emissions and removals distinctively quantified, thereby producing time series emission and removal estimates that are a meaningful, sensitive measure of corporate GHG performance, such as internal mitigation measures taken to achieve emission inventory reduction targets. For Scope 2 indirect emissions and other activity pool source categories deemed to be within a company’s Physical Inventory accounting boundaries, an average emission factor for that pool is to be used (e.g., geographic and temporally representative “location-based” grid average emission factors for electricity consumption). The use of an activity pool average factor is justified because any other allocation of emissions would entail a company making an exclusive claim on the emissions rate from particular sources in that pool, even though they have no exclusive physical connection to justify that claim. Therefore, a Physical Inventory statement should exclude any adjustments to inventory emission (or removal) estimates through EACs or other market-based approaches; the impacts of EACs and other market-based interventions are instead accounted for under the Mitigation Intervention or Non-GHG Transition Indicator statements.

The accounting for most market-based approaches is done under the Mitigation Intervention statement instead of the above Physical Inventory statement or some other kind of market-based inventory. The impacts of corporate interventions are estimated using physical consequential GHG accounting methods. This statement provides a standard for companies to report on the avoided emissions and enhanced removals resulting from “recognized ambitious” interventions.11 For example, corporate interventions via PPAs, REC markets, and other financial and contractual actions in electric power markets would require methodologies to be developed that estimate, with an acceptable level of uncertainty, ex-post avoided emissions impacts.12 Under the Mitigation Intervention statement, the sources and sinks affected by market-based interventions can only be reported on by a given company if they are outside that company’s Physical Inventory boundaries or in an activity pool (i.e., emission sources part of an electrical power grid). As a result, there is no double-counting of the effects of mitigation actions taken by a given company between the two statements.131415

The third statement—non-GHG metric transition indicators discussed in Installment N.7—is bespoke to each industry. Transition indicators could be appropriate for companies within the electric power industry (e.g., percentage of generation from corporate assets produced by low or zero-emitting technologies). Transition indicators should focus on physical actions taken by companies to transform their operations, including material consumption and product production, in a manner that is in keeping with a global net-zero emission pathway. For some industries and products, there could be a role for a market-based non-GHG indicator based on EACs. For example, the percentage of fuel-burn matched with SAF certificates for companies in the commercial aviation industry.

Market-based approaches have no role in the Value Chain Analysis discussed in Installment N.7, whose primary purpose is to help identify products likely to be in a company’s value chain that can be prioritized for investigation for pointed mitigation actions in upstream or downstream processes associated with those products. The ex-post impacts of actions taken to mitigate these emission sources in a company’s value chain would then be quantified and reported under the Mitigation Intervention statement. The integration of market-based accounting in this statement would obscure data needed to fulfil this purpose.

How should we report on market-based approaches within a multi-statement framework?

Ideally, it would be easy for companies to report perfectly accurate GHG impacts of their market-based actions using consequential GHG accounting methods. However, such a quantification may be infeasible (i.e., too much uncertainty) and/or impractical (i.e., analytically too difficult). For some market-based interventions—such as procuring “green” concrete or steel—non-GHG transition indicators may be a more appropriate metric and basis for establishing an EAC market than requiring each company to quantify and report avoided emissions. Different industries and types of market-based approaches call for different reporting approaches—some warrant consequential GHG accounting at the overall market level, some can be individually quantified in terms of GHG impacts at the EAC transaction level, and others are better tracked and commodified (e.g., converted to EACs) through separate non-GHG transition indicators (e.g., percentage of low-carbon materials procured or sold). It is also an option for both metrics, GHG and non-GHG, to coexist in a reporting or target-setting program, where appropriate.

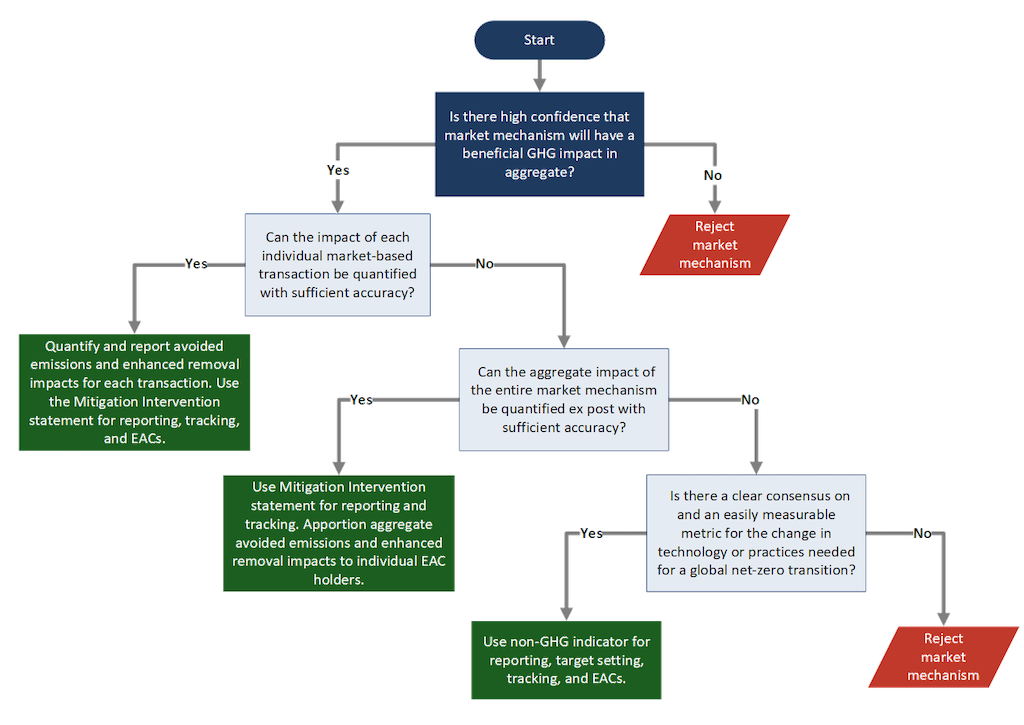

Figure 2 presents a decision tree for guiding the choice of how to adapt existing or treat new market-based approaches in a multi-statement reporting framework. Always, the essential first step is assessing whether there is high confidence that the market mechanism will have a large beneficial GHG impact in aggregate. If yes, the next step is evaluating whether it is methodologically practical to quantify the GHG impacts of individual transactions with sufficient accuracy, or whether this quantification is better done for the aggregate impacts of the entire market mechanism each year. For example, the former would likely apply to PPAs and the latter to hourly REC markets. In both these cases, intervention impacts are reported through the Mitigation Intervention statement. Although market incentives are best aligned with a first-best measure of GHG impacts, in many cases, it will be more practical to use a second-best proxy in the form of a non-GHG indicator. For example, we are highly confident that reaching global net zero will require a transition to green steel production (e.g., using hydrogen and/or carbon capture and storage), and so a market mechanism could be built upon a green steel production indicator. This option requires there to be an easy-to-measure and well-understood non-GHG indicator that can serve as a proxy metric and as the basis for establishing EACs or other contractual instruments.16

Figure 2. Decision tree for determining reporting of market-based approaches

Conclusion

The path forward for corporate GHG accounting should be clear if we loosen our status quo thinking straitjacket: we should abandon the flawed practice of using market-based approaches to manipulate inventory emission factors and instead develop a multi-statement GHG accounting framework that properly recognizes market-based instruments for what they truly are—mitigation interventions. By separating Physical Inventory from Mitigation Intervention statements and their respective reduction target and contribution goal setting, companies can be recognized both for energy efficiency improvements within their direct control and for their consequential impacts on broader energy markets through PPAs, hourly RECs, and other EACs. This paradigm shift eliminates many methodological contradictions that have plagued Scope 2 and Scope 3 accounting and directs corporate resources toward market-based activities that demonstrably reduce global atmospheric emissions rather than merely shuffling accounting allocations. The result will be corporate GHG reporting that serves the intended purpose of properly quantifying and recognizing meaningful climate action rather than frustrating it.

Annex A: Methodological problems with market-based inventory accounting

The Scope 2 market-based method has emphasized a “matching” framing of GHG inventory accounting—in other words, the degree to which a company’s electricity consumption is “matched” with market-based instruments, such as RECs, under the assumption that the financial transaction is a legitimate proxy for consuming energy from a specific renewable energy generator. Yet, as noted above, the logical purpose of a market-based approach is to have an aggregate mitigation impact, which is in keeping with the type of claim desired by companies. Market-based approaches that are justified by an MWh matching framing ignore the question of the EAC market’s impact, which could be large, small, or negligible. Therefore, it is essential to evaluate the overall market scale, the avoided emissions (or enhanced removal) impact of any market-based method through a consequential analysis. Because of this need to understand the impact of market-based instruments, as well as double-counting and “emissions shuffling” issues, there are several methodological problems created by the introduction of market-based approaches to GHG inventory accounting for direct and indirect emissions (i.e., Scopes 1, 2, and 3), which include:

How to construct residual average emission factors17 for activity pools (see Box 1), such as Scope 2 electricity consumption, to avoid double-counting of zero emissions between companies claiming RECs or other EACs and companies using pool average factors.

How to translate, in a credible manner, the avoided emissions impact of a market-based intervention occurring in or beyond a company’s value chain into an adjusted GHG inventory emission factor for use by that company in its GHG inventory. The consumption matching market-based method fails to evaluate whether and to what degree market-based actions are impacting overall GHG emissions, leading to a market that is dominated by low or no-impact EAC suppliers because they are the cheapest (i.e., the shuffling problem).

How to account for corporate interventions—both via market-based instruments and direct actions—in GHG inventory activity pools and supply sheds that have an effect on emissions and/or activity levels exceeding the quantity of the activity reported by the company.18

The need to deconstruct opaquely constructed LCA emission factors into detailed life-cycle processes so that those factors can be adjusted to exclude the exclusive market-based low and zero emissions attribute matching claims made by companies through EAC markets or other value chain interventions. This task is analytically complex, and in many cases, can only be done using unsupported assumptions (i.e., “guesswork”).

While the addition of a Mitigation Intervention statement escapes most of the problems with the current Scope 2 and emerging Scopes 1 and 3 market-based approaches (see Box A), there is one challenge that it shares. Both market-based inventory (i.e., consumption matching approaches) and a Mitigation Intervention Statement require solving the question of what EACs and other interventions are to be recognized in corporate GHG accounting.19 For example, we continue to struggle with establishing accepted criteria for Scope 2 EACs (e.g., RECs) that consider whether—and the degree to which—they have any avoided emissions impact. The form this debate is currently taking in the Scope 2 update process is around the eligibility constraints on the use of hourly RECs, which function as a proxy for constraining supply and furthering the additionality of the hourly REC market mechanism. A Mitigation Intervention statement faces a similar problem. However, because the Mitigation Intervention statement is built upon the application of consequential GHG accounting methods, unlike using EACs in GHG inventory accounting, addressing this challenge is inherent to the method. The consequential methods employed in this statement require the explicit establishment of credible baseline scenarios and a process for evaluating interventions made by companies, including those implemented through EAC markets, focusing on their avoided emissions and enhanced removals impacts. EAC markets that we have low confidence of having an overall beneficial impact should be omitted from the reporting statement. Applying such consequential methods—approved through a governance process—for each type of corporate intervention is designed to produce the kind of quantitative impact estimates that are absent from how EACs are treated in current corporate GHG inventories, which instead rely on an attribute-matching paradigm that suffers from the adverse selection “shuffling” problem.

Including market-based approaches in GHG inventories is an exercise of attempting to fit a square peg into a round hole. With the inclusion of market-based approaches in corporate GHG inventories, this challenge takes the form of determining the eligibility criteria for every EAC instrument someone proposes selling (e.g., RECs, SAF certificates, green steel certificates).20 Which EACs have enough GHG impact and broader environmental integrity to overwrite a company’s physical emission estimates? As we have found with the greenwashing criticisms of voluntary market RECs, this can be a vexing challenge. Imagine the same challenge multiplied a thousand times over by the need to address a huge marketplace of different types of EACs and contractual claims.

Box A. Summary of challenging GHG accounting steps when integrating EAC markets

Multi-statement framework including Mitigation Intervention statement

Develop and apply consequential impact quantification methods to estimate avoided emissions and enhanced removals for each market-based intervention and mechanism (e.g., EAC market)

Distribute the quantified impact claims to market participants (e.g., based on share of EACs held) for reporting in the Mitigation Intervention statement

Conduct a consequential analysis to determine the eligibility of each proposed EAC or other market-based instrument for use in inventory calculations to ensure it is likely to have a beneficial effect and not simply shuffle the allocation of emissions21

Determine whether the impact estimated for each market-based instrument is “enough” to warrant being used in GHG inventory calculation and replace the physically representative emission factor.22

Determine whether the market-based instrument impact claims are associated with sources or sinks that are traceable to the claiming company’s value chain to warrant replacement of its physical representative emission factor23

Develop and apply methods for adjusting the Scope 2 (or Scope 1 & 3) emission factor that is representative of the reporting company to account for market-based impact claims24

Develop and apply the method for generating “residual” emission factors that other reporting companies use, which adjusts the average emission factor for the exclusive source allocation claims of the companies using market-based instruments.

Acknowledgements

I am thankful for the insightful comments from and discussions with Tani Colbert-Sangree (GHGMI), Mark Trexler (The Climatographers), Alissa Benchimol (GHGMI), Matthew Brander (University of Edinburgh), Derik Broekhoff (SEI), Thomas Day (New Climate Institute), Bo Weidema (2-0 LCA), and other anonymous reviewers.

Recommended Citation

Gillenwater, M., (2025). What is Greenhouse Gas Accounting? Market-based approaches in multi-statement GHG reporting. Seattle, WA. Greenhouse Gas Management Institute, August 2025. https://ghginstitute.org/2025/09/03/market-based-ghg-accounting-multi-statement-reporting/

References

Brander, M., Bjørn, A., 2023. Principles for accurate GHG inventories and options for market-based accounting. Int J Life Cycle Assess 28, 1248–1260. https://doi.org/10.1007/s11367-023-02203-8

Gillenwater, M., (2023). What is Greenhouse Gas Accounting? Allocation rules. Seattle, WA. Greenhouse Gas Management Institute, October 2023. https://ghginstitute.org/2023/10/11/what-is-greenhouse-gas-accounting-allocation-rules/

I am grateful for the contributions of Gilles Dufrasne, Jonathan Crook, Injy Johnstone, Thomas Day, and Derik Broekhoff in developing earlier iterations of this multi-statement framework.

Even in the case where a market-based approach that is applied to corporate inventories is neutral in its effect (i.e., simply reallocates emissions between reporting companies based on a financial transaction) then in the context of a voluntary reporting and recognition program, it is having a negative impact because it is both incurring transaction costs and substituting for companies taking actions that actually reduce their physical inventoried emissions versus just shuffling emissions responsibility between entities.

For example, defining, registering, and policing tradable units; banking and borrowing provisions; addressing shifting emissions to uncovered entities; managing tradable unit supply and demand through issuance and usage rules to ensure overall market mitigation impact; and preventing market manipulation (e.g., gaming by market participants). The principles for these market design elements are related to policy efficacy and equity, in contrast to the more limited GHG inventory quality principles that are centered on accuracy and transparency.

During this period from roughly 2000 to 2015, almost all Scope 2 zero emissions reporting claims were based on the purchase of unbundled annual RECs (i.e., not in conjunction with a PPA) under short-term contracts (i.e., the precursors of today’s REC spot market).

The promise of increased impact with hourly RECs is expected to result from higher prices for RECs issued for hours exhibiting a supply scarcity (e.g., when solar and wind generation is less available).

There will be uncertainty in the estimation of the overall EAC market impact each year; however, some uncertainty is acceptable and unavoidable in any impact evaluation. Methodologically, this process is the same as ex-post policy impact evaluation, which has well-established methods. This process also highlights the importance of thoughtful design of each EAC instrument and EAC market rules so that its overall impact can be quantified and free riders are minimized. The current inventory attribute matching market-based approach mostly neglects these issues.

I do not address voluntary market annual spot market RECs or Guarantees of Origin (GOs), as research evidence indicates that in the absence of long-term contracts and upfront investment risk transfer provisions, these environmental certificate markets do not have an effect on renewable energy investment, and therefore, do not have an avoided emissions impact

However, significant work has been done in developing operating and building (short and long-run) marginal grid emission factors and methods for estimating the GHG impacts of renewable and energy efficiency projects.

A similar induced emissions analysis could be performed on a company’s other major upstream consumption and downstream production activities, with marginal consumption and production emission factors for these activities. In a future installment, we will propose to use such a comprehensive consumption and production-induced emissions metric as a reference for setting a corporate Mitigation Intervention contribution goal.

The baseline for estimated avoided emissions from mitigation interventions is a scenario in which that intervention was absent. As we will discuss in a coming report, only “ambitious” interventions that are clearly for the purpose of mitigating GHG emissions are accountable under the Mitigation Intervention statement. For an all consumption induced emissions value, the inverse is not the baseline, in that companies do not engage in emitting activities for the purpose of causing emissions.

A forthcoming installment in this series will elaborate on how to define and apply the “recognized ambitious” reporting eligibility principle for corporate “beyond inventory” mitigation interventions.

Interventions within GHG accounting activity pools, such as electricity consumption, could be reflected in both a Mitigation Intervention statement and fractionally in a Physical Inventory statement. For example, some portion of the impact of a corporate intervention in the electric power sector reported under the Mitigation Intervention statement could also have a small effect on the grid average emission factor using the same company’s Scope 2 indirect emissions reporting. We deem these minor cases of dual impact reporting across two separate statements an inherent artifact of activity pools that does not inhibit the use of each statement for appropriate intended uses because targets and goals, respectively, are applied based on each statement separately (i.e., the two statements, one on emission and the other on avoided emissions, are not summed to produce a net physical metric).

Any GHG accounting framework that features indirect emissions will also feature overlapping accounting boundaries between GHG inventories across companies. And so, Company A’s reported avoided emissions under its Mitigation Intervention statement may also be reflected as a reduction in Company B’s GHG inventory, if Company B’s emission sources are affected by Company A’s intervention. It would be incorrect to view this as a form of double-counting because it occurs across different statements with separate targets/goals and different companies. This is one of the reasons why the avoided emissions reported under the Mitigation Intervention statement should be interpreted as a contribution, not compensation—a contribution to global mitigation that could also be a contribution to helping some other company, or country, reduce its inventoried emissions and achieve its target. This is a feature, not a bug!

In some cases, a company’s intervention could affect both sources outside and inside its inventory boundaries. For example, a nitric acid plant owner makes an intervention that causes farmers to use fertilizer more efficiently, which avoids the release of on-field N2O emissions. But this intervention also avoids consumption of nitric acid, some of which the plant owner may produce itself, and thereby reduces the plant owner’s Scope 1 emissions. By design, the Mitigation Intervention statement would exclude the portion of the intervention’s impact occurring from the sources within the intervening company’s inventory boundary. Only the avoided emissions from the other “beyond inventory” sources may be reported under the Mitigation Intervention statement.

It can be easy to err with the design of non-GHG indicators in a market mechanism. For example, RECs were adopted as a form of non-GHG indicator-based EAC for voluntary green power purchasing claims. Although a transition to zero-emitting energy is clearly on a global net zero pathway, the market mechanism failed the first choice in the decision tree—the market mechanism did not have a large beneficial GHG impact.

A residual average emission factor is the average GHG emission rate per unit of activity within an activity pool associated with the portion of that pool remaining after exclusively claimed emission attributes from the pool are removed from the average calculation. In the context of Scope 2 electricity indirect emissions, it is the average GHG emission rate per unit of electricity (e.g., kg CO₂e/MWh) associated with electricity generation within a given geographic boundary and time period that is not associated with exclusively claimed emission attributes. Typically, it reflects the remaining grid mix emissions after accounting for all electricity attributes that have been claimed through market-based instruments such as renewable energy certificates (RECs), guarantees of origin (GOs), or power purchase agreements (PPAs).

For example, imagine a processed food product manufacturer that conducts an intervention to support more efficient fertilizer usage by a broad community of farmers in a growing region. These farmers produce a large volume of numerous crops, only a fraction of which are expected to be in the intervening company’s actual supply chain. Under the current expansive Scope 3 value chain inventory thinking, a complex calculation would need to be conducted to estimate what fraction of this agricultural production supplies the intervening company, and then an adjustment to the intervening company’s LCA emission factor for crop purchases would need to be developed to claim the partial impacts of the intervention that can be allocated to the intervening company. The other avoided emission impacts from the intervention would then either go unreported or could be reported as some form of “beyond value chain mitigation” by the intervening company. This complexity is an unnecessary result of problematically expansive and ambiguous Scope 3 boundaries!

Functionally, this is analogous to the question of baseline selection against which consequential impacts are evaluated (i.e., additionality). These eligibility determinations may need to consider regional differences and be updated regularly as technologies and circumstances change.

It may be expedient to integrate consequential impact methods for particular market-based claims into an allocational-style inventory GHG accounting protocol for the purpose of implementing specific policies that have clearly defined policy objectives. Such hybrid protocols are classified as performance GHG accounting, which means they produce neither a physical quantification of pure emissions nor avoided emissions. Performance GHG accounting is never policy neutral; it instead requires that a clear policy application and objective be specified to guide the construction of the performance scoring rules. An example of performance GHG accounting is the proposed GHG accounting rules for “green hydrogen” for the clean hydrogen production tax credit under section 45V of the Internal Revenue Code. The fundamental purpose of the associated rules covering market-based claims on “green power” is to cause additional investment in renewable energy generation capacity through the actions taken by companies receiving the tax credit.

A major flaw in the current market-based Scope 2 method is that this step is not taken, so whether or how much EAC markets and different EAC usage eligibility rules impact GHG emissions is left unevaluated, leading to a race to the bottom in the market.

The current Scope 2 market-based approach, as well as the proposed hourly REC update, also neglects this step, which is essential to establishing the environmental integrity of the overall EAC market.

There is also the situation in which a company makes a market-based intervention that is initially deemed to target sources in its value chain, but then the company’s value chain changes, and the intervention no longer falls within it. Is the reporting company still permitted to claim the adjusted emission factor for a source no longer part of its value chain (i.e., within current Scope 3 boundaries)? Why would companies invest in value chain mitigation actions if there is a significant probability they will not be able to claim and report on it unless their value chains unrealistically remain static over time?

This step is often analytically intractable for Scope 3 when LCA emission factors are used. Most market-based interventions will affect only one part of a product life cycle. Yet, these LCA emission factors are very rarely disaggregated by different emitting processes within each life cycle stage. Instead, they are presented as one aggregate life cycle value. Therefore, the data is rarely available to know how to adjust these LCA emission factors to account for changes in just one emitting process in that life cycle.

I do agree that a separate line of thinking is needed around just what are ‘market-based instruments’ as they are certainly not all created equal and as consequence have very different roles. For example, a bundled REC purchased from your supplier (or maybe an unbundled REC from a supplier on your grid) is really another form of supplier-specific arrangement that counts directly in your value chain. Whereas buying “green” steel credits from an unrelated supplier could be a half-way house to claiming you are addressing your own steel purchases, but risks the claim that you are ignoring investment in you own steel supply chain. Further, buying “credits” for wholly unrelated activity outside your value chain has a different purpose altogether.

In a world where a value chain has vague areas and whose vague areas likely change from month-to-month and year-to-year it seems attractive indeed to buy the cheapest arbitrary “market-based” instrument instead of figuring out the detail in the vagueness. Or just cut the vagueness out altogether. However, this would imply that *no-one* is tackling the vagueness and hence we will likely just end up with a different form of green-washing accusation – “you’ve changed the accounting rules to avoid making hard decisions”.

What I would like instead is a form of inventory statement that acknowledges what is vague and what is more certain – and addresses these appropriately. For example, it might be perfectly fine to buy general market “green steel” credits to match my actual spot-market purchase of steel. I’m reflecting a vague inventory boundary with an appropriate “activity aligned instrument”.

Thanks for engaging on this issue. Although I would strongly disagree that anything being proposed here is avoiding making hard decisions. Actually, I would reverse that charge back at anyone supporting more status quo thinking. There is a desire to perpetuate the fantasy that we can keep morphing a corporate inventory to do so many different things without really explicitly designing it to do anything specifically. Most importantly, it is to admit and recognize that a market-based approach is an exercise in designing a market-based mechanism with the purpose of having a mitigation impact on a market scale. The purpose of a market-based approach is not to improve inventory accuracy. Until that is admitted and we structure our debates accordingly, we will continue being stuck. Because framing choices about the design of market-based approach as an inventory methodology issues leads you to ask the wrong questions. While placing it in the context of a consequential method statement forces you to ask the correct design questions.

This article provides a thought-provoking critique of current GHG accounting practices, particularly the use of market-based approaches. I appreciate the clear distinction between physical inventories and mitigation interventions, though the complexity of implementing such a framework remains a concern.manus pricing

I would argue that the current GHG accounting framework is also very complex. Ask anyone who is trying to prepare an estimate of Scope 3 emissions, interpret it, and use it in any meaningful manner. Again, NO company anywhere even knows the sources and sinks in its value chain / Scope 3. But there is a real issue with a transition to a better GHG reporting framework. I would argue, though, that the cost of the status quo, in the form of ongoing wasted resources and ineffective action due to ineffective recognition metrics, is far far greater than one-time transition costs to something more effective. I don’t buy the argument that the status quo is working…nor do I buy the argument that we can just make minor tweaks and all will be better. The problems are deeper than that, which is why this “What is GHG accounting?” series of installments has gone back to the fundamentals to diagnose the problems and then derive solutions to those structural faults.

Comments