Installment N.6

Introduction

This post continues our “What is Greenhouse Gas Accounting?” series, which explores fundamental questions in corporate greenhouse gas (GHG) accounting. If you have not read the series, all installments are available here. They provide necessary context for the issues explored in this post. Of particular relevance are the installments on the flaws in the application of Life Cycle Assessment (LCA) to Greenhouse Gas (GHG) accounting and how to understand the rules for allocating emissions to companies used for preparing GHG inventories.

This installment specifically elaborates on “Is Scope 3 Fit for Purpose?” written with Derik Broekhoff. Within that installment, we discussed how to address the flaws in the GHG Protocol’s approach to setting the Scope 3 boundary. We argued for a narrower and more intentional approach to the allocation of GHG emission sources and sinks to companies that will result in meaningful estimates of indirect emissions over time, establish an unambiguous standard for completeness, and enable the production of comparable[1] emission totals across companies in the same industry[2]—qualities the current GHG Protocol corporate standards do not achieve. But, in that installment, we did not elaborate on how to set these narrower and more intentional indirect emission and removal accounting boundaries for physical GHG inventories (what we referred to as “Framework #1”). I address this key question here.

In the “Is Scope 3 Fit for Purpose?” installment, we proposed the use of two separate GHG accounting frameworks for corporate reporting—one based on a Physical GHG Inventory statement using allocational methods and a second based on a Mitigation Intervention statement using consequential methods. Key differences between these two frameworks are summarized in Table 1. A pivotal benefit of shifting to multiple separate statements, rather than the current sole reliance on a corporate GHG inventory report, is that multiple statements would help suspend conflation and the resulting confusion between allocational and consequential GHG accounting claims that is exhibited by the current corporate GHG Protocol paradigm.

Table 1. Summary of two GHG accounting frameworks for corporate GHG reporting statements

| Property | Physical Inventory | Mitigation Intervention |

|---|---|---|

| GHG accounting subject (who or what?) |

Entities with clear source & sink allocation boundaries | “Recognized ambitious” interventions |

| Type of quantity estimated (how much?) |

Emissions & removals | Avoided emissions & enhanced removals |

| Accounting boundaries |

All physically identified emission sources and removal sinks that the subject of GHG accounting is deemed responsible for | Emitting or removing processes altered (including additions and subtractions) by the intervention, while processes unchanged are excluded |

| Changes are measured relative to… | Previous time period (annual) totals | Non-intervention baseline scenario over the same time period |

| Intended use (why?) |

Corporate inventory target setting and tracking | Corporate “beyond inventory” contribution goal setting and tracking3 |

| Type of quantification method (how?) |

Allocational method | Consequential method |

A crucial design element of the improved Physical Inventory statement is its requirement for “clear” GHG accounting boundaries that explicitly identify physical emission sources and removal sinks included within a company’s GHG inventory, which is not a requirement satisfied by the current approach to indirect emissions under the GHG Protocol corporate and Scope 3 standards.[4] This is done through the application of industry-specific (i.e., sector-specific) boundary-setting rules. A shift to such a Physical Inventory statement, therefore, will require further work to determine, for each industry, what processes (i.e., sources and sinks) are to be included within standardized industry boundaries to advance the principle of comparability across companies within the same industry. This installment proposes boundary-setting principles to guide the establishment of industry-specific boundaries and briefly discusses how to approach this work, given the wide range of different industries.

What are “clear” boundaries?

In place of the ambiguously expansive and massively overlapping[5] GHG accounting boundaries envisaged by the current approach to Scope 3, a Physical Inventory statement intentionally identifies specific emission sources and sinks within processes in a manner that advances comparability across companies within a given industry. By delimiting boundaries to sources and sinks, which can be physically identified by a reporting company, including for indirect emissions and removals, the accuracy, time series consistency, and sensitivity of estimated indirect emission totals can all be enhanced. Transforming a corporate GHG inventory in this way can produce meaningful and comparable trends over time.

More broadly, this transformation entails establishing a new, multi-statement corporate reporting framework intentionally designed to achieve accountability for GHG emissions at the individual company level, while also providing a more effective basis for recognizing company-specific performance. Two key elements of improving accountability are: i) ending the collective and ambiguous assignment of responsibility for emissions to companies that is embedded in the current approach to Scope 3,[6] and ii) producing an improved metric—in the form of a Physical Inventory time series—that produces indirect emission and removal estimates that are truly sensitive to both actions taken by a company and real-world changes over time. Beyond fostering accountability, a further benefit of this transformation will be the redirection of resources, including staff time and attention, from estimating life-cycle emissions to the imagined ends of complex value chains and creating certificate-based workarounds, toward ambitious, value chain-focused interventions. The reporting of the GHG impacts of interventions can be separately recognized and accounted for under a Mitigation Intervention statement designed to credibly quantify the avoided emissions impacts of corporate actions.

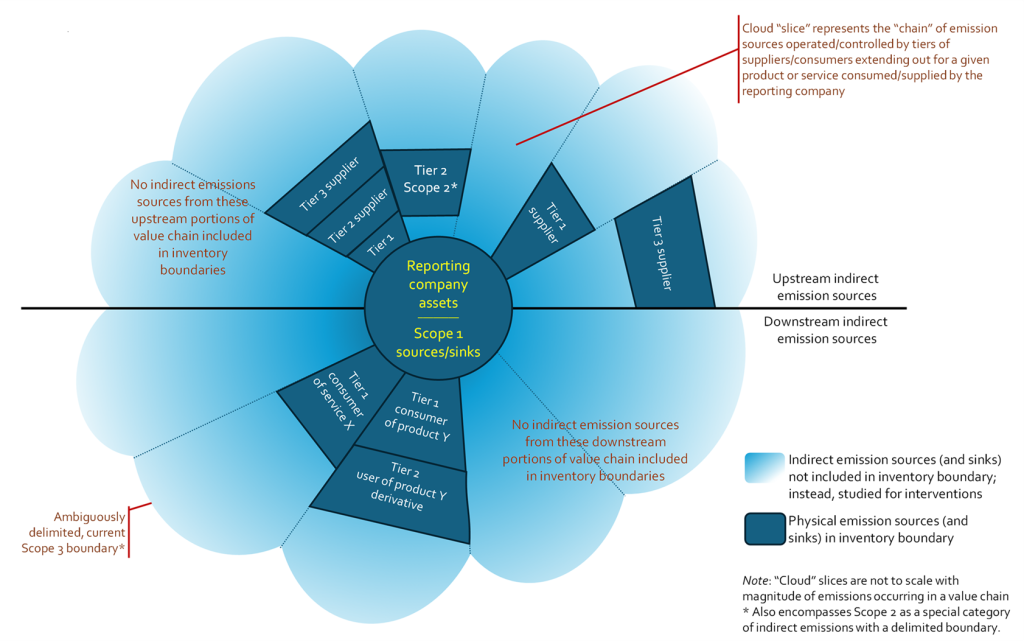

Our previous post conceptually illustrated this transformation from ambiguously expansive value chain boundaries to intentionally delimited Physical Inventory boundaries (Figure 1).[7] We also introduced a Mitigation Intervention statement (referred to as Framework #2) that quantifies the impact of interventions that avoid emissions (or enhance removals) at sources (or sinks) located outside the delimited Physical Inventory boundaries. Although these impacts may still be within a company’s perceived value chain, they are deemed “beyond inventory.” The underlying transformation here is to detach the amorphous concept of a value chain from the definition of physical inventory. The obvious question, then, is: what are the principles for an intentional selection of processes, with specific sources and sinks, to include in delimited Physical Inventory boundaries for each industry (i.e., how to select the dark blue trapezoids in Figure 1)? The overarching intention is to construct efficacious boundaries, not to permit companies to dodge responsibility.[8]

Figure 1. Illustration of a precisely delimited allocational GHG accounting framework for corporate inventories. The cloud represents the expansive life cycle concept of “all” indirect emissions (i.e., Scope 3 as well as Scope 2) that a company is assigned responsibility for under existing corporate GHG accounting guidance. The line bisecting the cloud distinguishes upstream versus downstream indirect emission sources and sinks. The circle at the core represents a company’s direct emissions sources (i.e., its owned or controlled assets). Each illustrated “slice” of the cloud represents the emission sources from the chain of downstream or upstream suppliers or consumers (the tier of supplier represents its proximity to the reporting company in the specific product line ‘slice’; a Tier 1 supplier directly engages with the reporting company), respectively, for a given consumed input or produced output product or service.[9] The darker colored trapezoids indicate the selected emission sources that are included in a more precisely delimited corporate Physical Inventory boundary, which only includes upstream and downstream sources and sinks selected to achieve comparability across companies in the same industry.

Principles for Physical Inventory boundary setting

The following Physical Inventory “operational” boundary setting principles recognize that even within a given industry, companies vary in how they are structured, and so the principles focus on identifying physical processes—and their emitting sources and sinks—common to a given industry, regardless of whether they correspond with direct or indirect emissions for a given company. Instead of each company independently creating its own bespoke corporate inventory boundaries implied through spend-based activity data, the approach proposed here would develop common boundary-setting rules for all companies in the same industry. The following corporate Physical Inventory principles are proposed for developing a separate boundary standard for each industry that explicitly specifies the processes included in that boundary:

- Pursue intra-industry comparability. Physical Inventory boundaries for a given industry should extend far enough to allow emission totals to be comparable between a company that maximally outsources processes and one that maximally insources, such that totals and emission trends across companies are not significantly biased by variations in corporate structure. Indirect emission sources (or sinks) that are beyond what any maximally vertically integrated company within that industry would sensibly include within its organizational (Scope 1) boundaries (e.g., a maximally “insourced” company) may be considered for exclusion from boundary-setting rules for that industry.[10]

- Limit to proximate physical connections. Indirect emission sources or sinks that have a very distant physical flow connection (i.e., traceability challenges) with the reporting company’s owned or operated (i.e., Scope 1) processes should be excluded from the Physical Inventory boundaries for an industry (i.e., concentrate GHG accounting more on Tier 1 & 2 suppliers versus Tiers 5, 6, 7, and beyond).

- Process-level visibility and quantifiability at the process level. Processes with sources and/or sinks should not be included in Physical Inventory boundaries for an industry if it would be impractical for most reporting companies, unless in exceptional circumstances and with extreme effort, to identify those sources and sinks and collect process-specific data (i.e., primary activity data and representative emission factors).[11]

- Screen for significant source and sink categories. Physical Inventory boundaries for an industry should be further screened to only include sources and sinks with large emissions or removals (i.e., high emissions intensity processes) relative to the total Scope 1 emissions of a typical reporting company in that industry.

- Sectoral additivity. Optionally, Physical Inventory boundaries for an industry may be set so that there is no, or minimal, duplicative assignment of emissions or removals across companies (i.e., no double counting) within the same industry or sector (i.e., same population of companies).[12] The outcome of doing so is that accountability at the individual company level is heightened, and inventory emission totals for each reporting company can be summed to produce industry or sector totals (i.e., additivity) of participating companies. Such an aggregated sectoral metric can be valuable to industry associations that wish to commit to and track sectoral targets, determine burden sharing for policy making, and/or prepare benchmarking estimates, something that the current approach to corporate reporting does not enable.

Given that these principles are not objective rules that will produce definitive boundary classifications and that trade-offs may be necessary between principles, there will be processes with indirect emission sources and sinks in which debate exists over whether they should be classified as within or beyond the Physical Inventory boundary for a given industry. For these cases, it is also appropriate to consider the role of other corporate GHG reporting statements within a multi-statement framework. For example, is the process in question a prospective subject for an “ambitious” and “quantifiable”[13] intervention by companies in the given industry? Additionally, are there serious doubts about whether the process in question is both visible and quantifiable by reporting companies in that industry? If the answer to these two questions is “yes,” then it is recommended that the process be excluded from Physical Inventory boundaries for that industry and instead be addressed through a Mitigation Intervention statement. If the answer to both questions is “no”, then the process should be included in the Physical Inventory boundaries for that industry. If the answers are mixed, then expert judgement will need to be applied.

Physical allocation of Scope 2 and other activity pool indirect emissions

Scope 2 is an activity pool emission source category.[14] These Scope 2 indirect emissions from acquired and consumed energy will satisfy the above boundary-setting principles for almost all companies and, therefore, should be included in Physical Inventory boundaries. Other activity pool indirect emissions sources (e.g., indirect GHG emissions from fuel combustion for bulk shipping of a consumed product, indirect N2O emissions from fertilizer used for commodity agricultural production of a consumed product) should be selected for inclusion in or exclusion from an industry’s Physical Inventory accounting boundaries based on the same five principles above. Activity pool emissions should be allocated to individual companies based on pooled average emission factors per unit of their physical share of consumption or output (e.g., mass or energy unit share, grid average) (see Box 1). Ideally, Scope 2 grid average emission factors will have a high degree of temporal and spatial representativeness of the company’s physically accessible activity pool supply. Updates to the GHG Protocol Scope 2 guidance should focus on improving the location-based methods.

Box 1. What is an activity pool?

| In the context of allocational or GHG inventory accounting, an activity pool is defined as a common set of emission sources whose processes physically serve (i.e., are connected to) an accounting subject (e.g., company) where traceability from the specific physical source of emissions to a specific accounting subject is not possible (Brander and Bjørn, 2023). The most well-known activity pool is a shared electricity distribution grid, along with the generators connected to it. But other examples include natural gas pipeline networks, agricultural and raw material commodities, and waste management systems used for the disposal of sold products. Because consumption or production of products or services by companies from an activity pool is from a mixture that cannot be differentiated with respect to its upstream or downstream processing, emissions are logically allocated based on the average emissions intensity (i.e., emission factor) of that pool. Any other allocation rule would presume exclusively physical traceability exists, when in truth it does not, or would allow emissions to be reallocated between companies based on purely financial or contractual arrangements. |

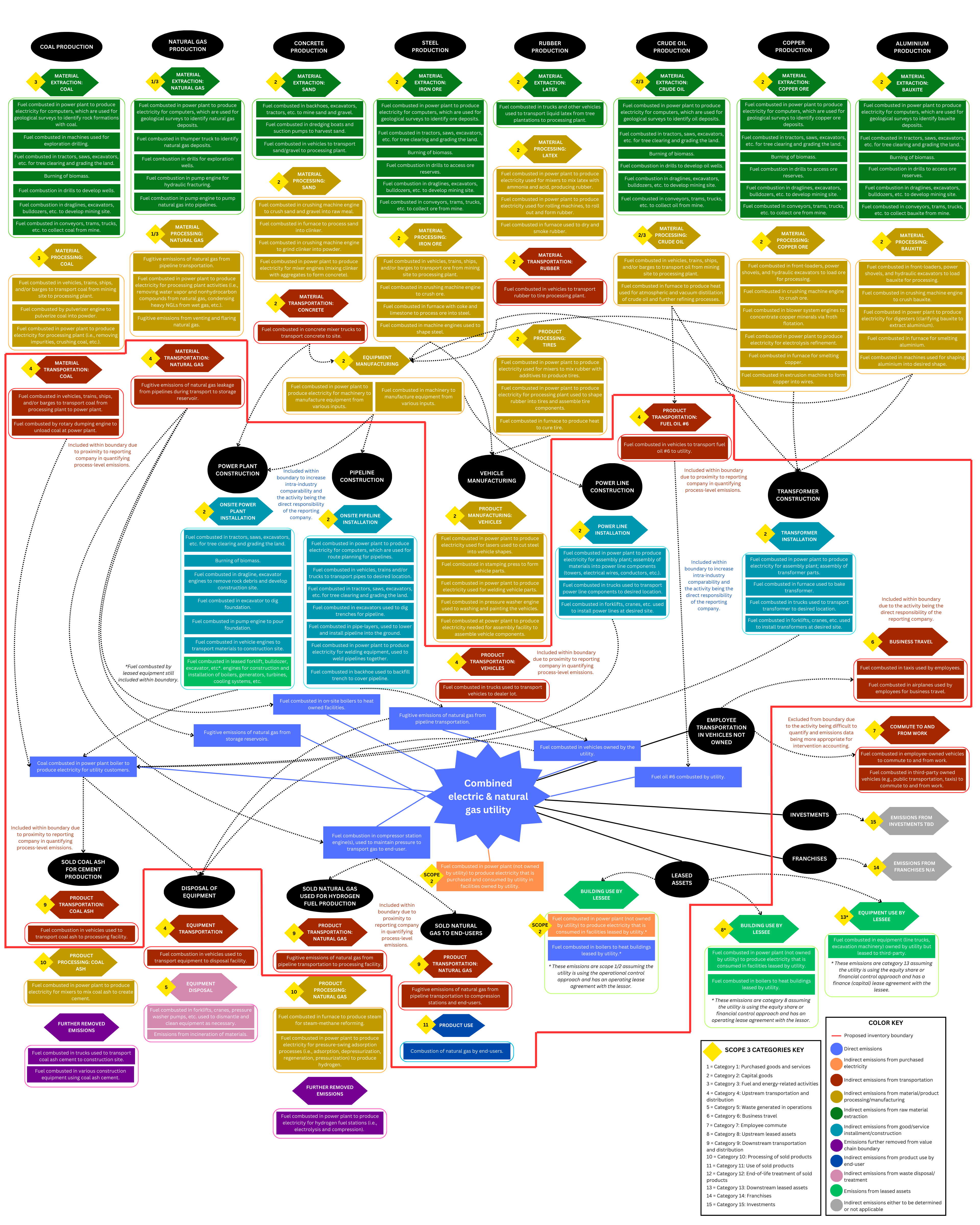

Boundary setting example

Figure 2 provides an illustrated case study example for the application of these principles to a combined electricity and natural gas utility.[15] We have attempted to present a modestly expansive elaboration of the value chain of this type of utility company. Yet, even all the numerous processes illustrated in this figure do not definitively extend to the undefined limits of the value chain for such a company. Because there is no objective definition of a “complete” accounting of a value chain, such a determination of completeness, in keeping with the Scope 3 standard, is subjective. The point of this example is to illustrate how Physical Inventory boundaries could be specified in an objective and comparable manner by clearly denoting which specific emitting sources are included, regardless of whether they are labeled as direct or indirect for a given company, and which sources are excluded. A Physical Inventory approach to corporate GHG accounting, as illustrated in Figure 2, can fulfill the objectives of transitioning away from the current problematic value chain-based approach to boundary setting discussed above.

Figure 2. Click on the image to expand. Example of a precisely delimited corporate Physical Inventory boundary for the combined electric and natural gas industry (Graphic credit: Erika Barnett, GHGMI)

For example, in Figure 2, we excluded from the Physical Inventory boundaries emission sources occurring in processes involved in the material extraction of raw materials—such as coal, steel, natural gas—because i) it is unlikely for utility companies to vertically integrate to control/operate mining operations associated with these resources, even though they may be considered within their value chain, and 2) utility companies are unlikely to have process-level data this far upstream.[16]

A straightforward illustration of these boundary-setting principles involves a company engaged in cotton cultivation. Downstream, other companies purchase this cotton to manufacture textile products, such as socks, which are ultimately used and repeatedly washed by end-use consumers. Under a Physical Inventory framework that applies these principles, CO₂ emissions from hot water production in gas-fired residential water heaters used to wash these socks would not be allocated to the cotton farming company, even though such consumer activities fall within its downstream value chain.[17] No cotton grower would plausibly vertically integrate into the manufacturing or operation of washing machines and water heaters merely because some of its cotton ends up in laundered consumer goods. Furthermore, the cotton producer is unlikely to have process-level visibility into appliance manufacturing facilities or consumer usage behaviors, and therefore would be unable to obtain the data required to estimate these emissions with any reasonable accuracy.

How to transform into “visible” Physical Inventory boundaries?

In the context of corporate GHG reporting and leadership recognition programs, a transformation to Physical Inventory accounting boundaries that improve accountability will entail transition costs. Substantial work will be required to establish industry-specific boundaries, and governance will be necessary to oversee this work across various industries. While some of this work may be managed by cross-cutting standard developers, such as the GHG Protocol, it would be more effective and expedient for the bulk of the work to be undertaken through a bottom-up approach involving industry associations, independent research centers, and environmental organizations with technical expertise that are dedicated to specific industries. The resources of cross-cutting standard setters like the GHG Protocol would be better directed at the onset to provide detailed guidance applicable to all industries (including an industry classification taxonomy). Subsequently, standard setters should review and adopt—or reject as gatekeepers—the draft outputs of each industry working group.[18] These drafts must include detailed technical justifications that reference cross-cutting guidance for the proposed boundary recommendations to be accepted.

To facilitate this bottom-up boundary setting process, the GHG Protocol and/or other standard-setting organizations should establish an initial taxonomical disaggregation of industries that are expected to each have their own boundary setting rules. A useful starting point would be to base this taxonomy on extracts from existing industrial categorization schemes, including the ISIC (International Standard Industrial Classification), the European NACE (Nomenclature of Economic Activities), and the NAICS (North American Industry Classification System).[19]

Conclusion

This installment has outlined principles for setting industry-specific boundaries within a Physical Inventory GHG accounting statement, offering a methodologically rigorous alternative to the expansive and opaque treatment of indirect emissions under Scope 3. By anchoring inventory boundaries in physically identifiable process-level emission sources and sinks, this transformation can produce corporate GHG inventory totals and trends that are more accurate, comparable, and sensitive to real changes in corporate operations and decisions. When paired with a separate Mitigation Intervention statement to account for consequential impacts of corporate interventions outside these improved Physical Inventory boundaries, such a multi-statement reporting framework offers more meaningful quantitative corporate GHG time series metrics. These proposed principles for Physical Inventory boundary setting can properly support comparisons across companies, target-setting, and performance tracking, as well as other intended uses of corporate GHG reporting.

Lastly, the corporate GHG accounting community must finally confront the fundamental question of comparability across corporate GHG reports with honesty and openness. For example, the assumption that choosing to buy from or invest in a company with lower reported GHG emissions will lead to real-world reductions of total global emissions to the atmosphere is fundamentally a consequential question, not one resolvable through sub-global inventory estimates. Likewise, a lower reported GHG inventory provides an extremely weak proxy for an individual company’s global net-zero transition risk exposure. If comparability across companies is to be an objective for a particular use case of corporate GHG reporting, then the applied standards and methods must be purpose-built to produce the desired level and form of comparability that supports that use case. Alternatively, as a community, we could choose that comparability is not to be a valid feature of corporate inventory reports. But then this stance must, at long last, be clearly and prominently communicated to all users of corporate reports. What cannot be accepted is the tacit perpetuation of a comparability illusion, wherein GHG Protocol-compliant inventories are used for comparative decisions despite lacking the methodological foundation to support such use, thereby enabling misinterpretation and misuse of reported data. The proposed reforms presented in this installment aim to address use cases where comparability is necessary and desirable.

Read all the Posts in the “What is GHG Accounting?” SeriesAcknowledgements

I am thankful for the intrepid value chain mapping and graphics works of my colleague Erika Barnett (GHGMI), as well as the insightful comments and discussions with Matthew Brander (University of Edinburgh), Derik Broekhoff (SEI), Erika Barnett (GHGMI), Alissa Benchimol (GHGMI), and Tani Colbert-Sangree (GHGMI).

Recommended Citation

Gillenwater, M., (2025). What is Greenhouse Gas Accounting? Towards comparability by fixing the Scope 3 boundary problem (Installment N.6). Seattle, WA. Greenhouse Gas Management Institute, May 2025. https://ghginstitute.org/2025/05/27/what-is-ghg-accounting-toward-comparability-by-fixing-the-scope-3-boundary-problem/

References

Brander, M., Bjørn, A., 2023. Principles for accurate GHG inventories and options for market-based accounting. Int J Life Cycle Assess 28, 1248–1260. https://doi.org/10.1007/s11367-023-02203-8

[1] What makes two entities comparable? Entities are comparable if they share a set of common properties that allow them to be analyzed and highlighted for differences across other properties. If two entities belong to entirely different populations (e.g., types of companies) that lack shared properties, they are not comparable. However, comparability does not mean that all aspects of two companies must be identical; rather, it means that the range of differences is sufficiently limited to allow for a meaningful interpretation of the differences present in the compared metric. [2] Throughout this blog, “industry” refers to a classification of companies engaged in similar activities. [3] Avoided emissions and enhanced removals reported are not intended to be used to make compensation (i.e., offsetting) claims against a company’s reported Physical Inventory GHG emissions. [4] Technically, there is nothing new about the Physical Inventory statement, as it simply proposes returning to the long-established practices in emissions inventory preparation, which involve defining emissions accounting boundaries by clearly delimited specific physical sources and sinks. It was the introduction of Scope 3 using life-cycle methods that deviated from this well-established technical norm in environmental engineering. [5] The GHG Protocol’s Scope 3 framework, by design, results in the non-exclusive allocation of emissions, whereby multiple companies report the same indirect emissions without any form of reconciliation of, or transparency on, the duplications. See here for a more in-depth discussion of this issue with Scope 3 reporting. [6] An effective accountability framework does not necessarily require the exclusive allocation of responsibility, but the number of entities allocated responsibility for a given emission source needs to be both small and clearly defined so that collective action can occur and information barriers can be overcome. An approach where a large, but unknown, number of companies, that are also mostly unknown to each other, are expected to all be accountable for the same emission source is not the basis for an effective accountability framework. [7] A rarely understood distinction is that the GHG Protocol standard on Scope 3 applies a concept of a value chain that is always relative to and different for each reporting company, versus in economics where a value chain is typically defined relative to the production of an economic good, and is therefore the same for every company in that chain. [8] Some will argue that the proposed principles presented here may be used by fossil fuel companies to “dodge taking responsibility” for downstream indirect emissions associated with the combustion of their products. Although this is not a given outcome of the boundary development process, the more relevant question is whether there is a useful use case for corporate GHG reporting by fossil fuel companies with a realistic theory of change associated with net zero and other recognition programs that leads to voluntary participation and major changes in the activities of fossil fuel companies. If such opportunities exist, then a multi-statement reporting framework could easily incorporate additional statements with industry-specific net-zero transition indicators, such as the quantity of carbon in fuels produced by fossil fuel companies for downstream combustion by end-use customers. If the use case is mandatory reporting and regulatory compliance, jurisdictions already have a well-tested and established approach to reporting downstream CO₂ emissions associated with the oxidation of the carbon content in the fossil fuels they supply that relies on facility level—not corporate GHG inventory—reporting by fossil fuel suppliers (e.g., refiners, importers, natural gas distributors). Examples include the U.S. EPA Greenhouse Gas Reporting Program, the California Cap-and-Trade Program, the Oregon Climate Protection Program, the Washington Cap and Invest Program, the European Union Emissions Trading System, and the New Zealand Emissions Trading System. [9] Note that some product or service line ‘slices’ in Figure 1 identify a Tier 2 or 3 supplier but do not include the lower-number Tier suppliers (for these ‘slices’, the Tier 2 or Tier 3 supplier is not directly touching the “reporting company assets” circle in the center). This represents a situation in which, for example, a Tier 2 supplier provides an input to a product line, and the Tier 1 supplier superficially processes that input; therefore, it is not considered to involve significant emission sources. [10] Section 5.2.4.3 of ISO 14064-1:2024 provides guidance on quantifying organizational GHG emissions, which also considers the impact of outsourcing on selecting indirect emission sources for quantification. [11] For the agriculture and land use sector, some of these sources and sinks will be “area sources,” which refers to a diffuse source of emissions spread over a specifically identified geographic area, rather than a single, identifiable point. [12] The very nature of reporting indirect emissions means that there will be duplicative reporting of emissions across all companies. Additivity, as described here, is intended only for companies within the same industry that apply the same boundary-setting rules. [13] The intervention eligibility principles “ambitious” and “quantifiable” will be elaborated on in a forthcoming installment of the “What is GHG Accounting?” series. [14] Scope 2 is a good example of more clearly delimited boundaries for indirect emissions that specify what emitting processes are within the boundary (i.e., fuel combustion for energy generation vs. the entire life cycle of electricity production and/or consumption). [15] This case study is not intended to indicate definitively what the boundary setting rules for electricity and natural gas utilities, as an industry, must ultimately be defined by a Physical Inventory corporate GHG accounting standard. Further work and consideration by industry experts is called for, as well as consideration of the different intended uses these companies will seek to fulfill by applying the standard. [16] Some utilities with coal-fired generation units are known to own and/or operate coal mining operations, and so are vertically integrated up through mining operations. An approach to these cases could be to treat mining operations as a separate business unit, categorized within the boundary-setting rules for the mining industry. [17] Replace the cotton farmer with a product retailer, such as Amazon or Walmart, and the argument is similar. [18] This cross-cutting guidance may need to vary by the different intended uses of corporate GHG reporting. [19] Further work is needed to explore the level of industrial classification disaggregation that is most appropriate for different intended uses (purposes) of corporate Physical Inventory reporting, such as 3-, 4-, or 6-digit industry codes.

Cover image from Wikimedia. Authored by the Greenhouse Gas Protocol, a joint initiative of the World Resources Institute and the World Business Council for Sustainable Development (WBCSD), it is part of the Climate Program. This image is under a compatible license; the information can be found on their website under the “Research” tab: https://www.wri.org/research/permissions-licensing. https://www.wri.org/initiatives/greenhouse-gas-protocol

Comments