What is GHG Accounting? Paradigm shift to multi-statement GHG reporting (Installment N.7)

Executive Summary

The Problem

Current corporate greenhouse gas (GHG) accounting, engulfed by Scope 3 reporting under the GHG Protocol, has created a dysfunctional system that frustrates rather than facilitates meaningful corporate climate action. The existing framework suffers from the following critical flaws:

Reliance on a single metric: A “full” corporate value chain inventory is expected to serve multiple distinctive purposes—accountability, performance tracking, risk evaluation, and mitigation impact recognition—when no single metric can effectively serve all these intended uses.

Unworkable boundaries: Current Scope 3 accounting creates overly expansive, ambiguous, and overlapping value chain boundaries that frustrate individual accountability, making it unrealistic for companies to accurately track, manage, and reduce “their” emissions through their own actions.

Compensation-based net zero: The current corporate net zero paradigm forces companies to rely on offsetting and other EAC market mechanisms to compensate for emissions they cannot meaningfully control, attracting greenwashing and moral attacks.

Product-based rather than source-based accounting: Scope 3 treats inventories as aggregations of product life cycle assessments rather than an accounting of identifiable physical emission sources, making it impossible for companies to target specific sources for mitigation.

The Consequences

The flawed existing corporate GHG reporting framework has trapped leading companies in a “doom loop” where they are simultaneously criticized for not taking full responsibility for indirect emissions and for greenwashing when they attempt to address these emissions through market-based mechanisms. The spend-based estimation methods that dominate Scope 3 reporting are insensitive to actual mitigation actions, creating a fundamental disconnect between corporate climate efforts and science-based recognition systems.

The Solution: Multi-Statement Reporting Framework

This installment of the What Is GHG Accounting series proposes replacing the single corporate value chain inventory with a four-statement reporting framework:

Physical Inventory Statement

Modified version of the current GHG Protocol Scope 1 and location-based Scope 2, and a narrowed Scope 3 that focuses on clearly identified physical sources and sinks

Narrower, unambiguous boundaries so that companies have clear visibility on the sources and sinks contained

Excludes market-based adjustments, providing clear accountability for inventoried emissions

Supports science-aligned reduction targets with a clear line of sight to emission sources

Mitigation Intervention Statement

New consequential accounting metric for “beyond inventory” and activity pool corporate interventions

Reports avoided emissions and enhanced removals from ambitious mitigation actions

Addresses the current insensitivity of Scope 3 to corporate mitigation efforts

Treats market-based mechanisms as intervention tools rather than inventory adjustments

Tracks progress on established decarbonization pathways (e.g., EV adoption in automotive)

Supplements GHG metrics with concrete transition measures

Value Chain Analysis

Maintains the current Scope 3 function for hotspot identification

Provides crude estimates to guide where companies should focus mitigation efforts

Updated only after major structural changes, not annually

No longer treated as a precise accountability metric

Key Benefits

This framework eliminates the core problems of current GHG accounting by:

Enabling clear accountability: Companies can set realistic targets based on emissions they can track with sensitivity and meaningfully control

Recognizing beyond-inventory action: Dedicated reporting for mitigation interventions farther out in value chains and beyond

Removing compensation paradigm: Eliminates problematic image of companies buying their way out of taking responsibility while maintaining ambitious expectations for internal mitigation and contributions to global mitigation

Improving metric sensitivity: Both inventory and intervention metrics quantitatively and credibly respond to the actual efficacy of corporate mitigation efforts

Maintaining broad responsibility: Companies remain accountable for wide-ranging upstream and downstream indirect emissions through different appropriate metrics

The Path Forward

Implementing this paradigm shift will require developing sector-specific boundary rules, establishing credible consequential accounting methodologies, and adapting existing target-setting programs. However, these implementation challenges are minor compared to the fundamental dysfunction of continuing with current approaches. The stakes are high—climate action demands deeper and wider corporate participation, and our current accounting framework is impeding rather than enabling the very action we need.

Introduction: Bad assumptions blocking our path

Imagine a future in which the vast majority of resources companies, universities, and other organizations spend addressing greenhouse gas (GHG) emissions are directed toward implementing and tracking mitigation actions that are recognized as making a meaningful climate difference.1 In this future, validly reported actions would not be perceived as greenwashing nor moral evasion of corporate responsibility because their beneficial impact would be generally respected. Imagine the intense debates and uncertainty over corporate recognition and accountability for GHG emissions and meaningful mitigation actions finally settled. Imagine GHG accounting rules, methodologies, and tools that are well-established, practical, and yield sufficiently credible results without being unrealistically burdensome to apply. Such a vision should not be a fantasy; it should be our expectation. But to get there, we will need to rethink some outdated assumptions and let go of a status quo shaped decades ago when our understanding of and applications for corporate GHG accounting were immature.

The key outdated and dysfunctional GHG accounting assumptions blocking our path to this future are summarized below, as well as some recommendations for how to retool our thinking.

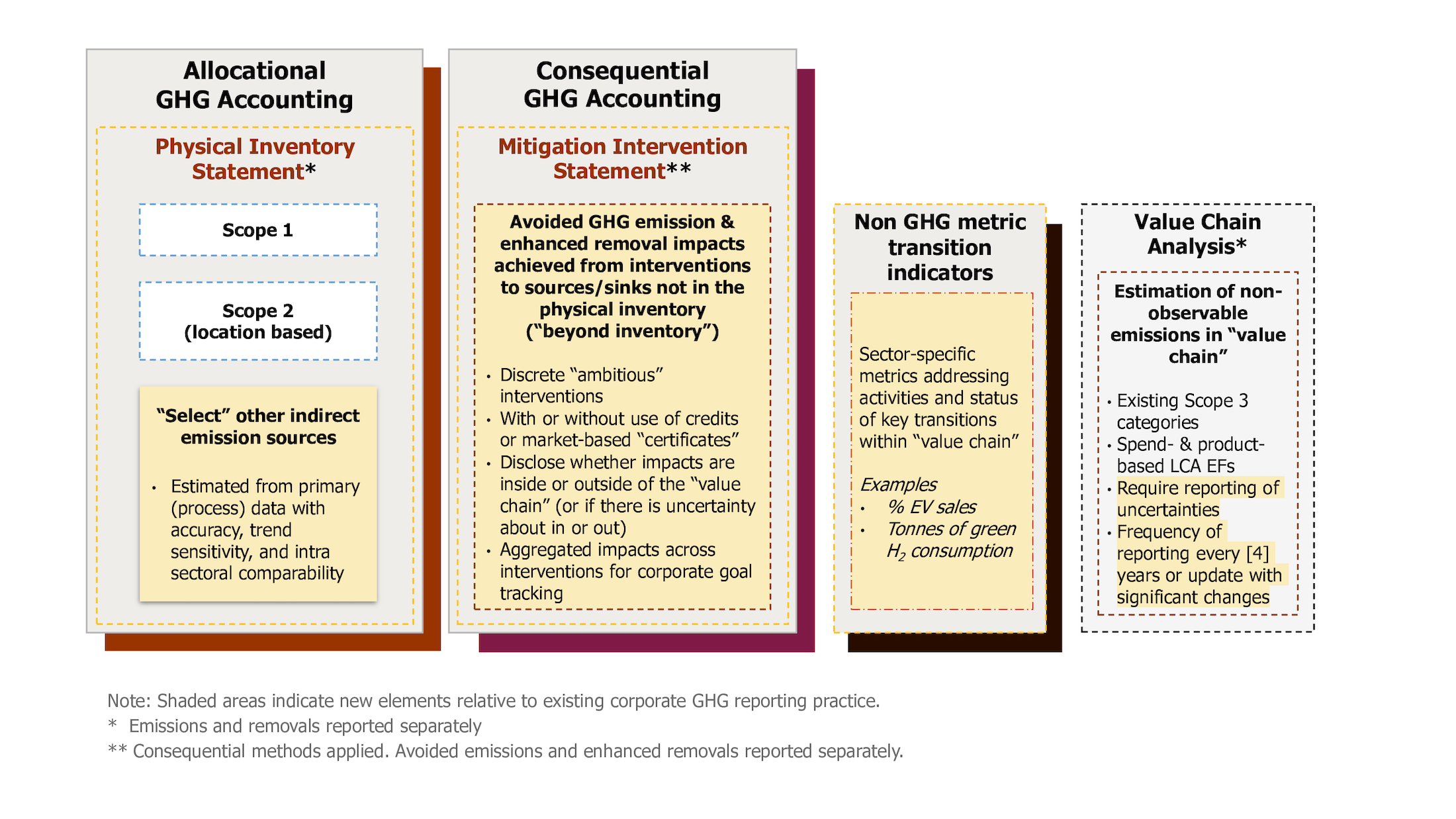

1.) A single metric—in the form of a “full” corporate value chain GHG inventory—is suitable for fulfilling numerous different purposes related to corporate GHG accountability and performance tracking, climate risk evaluation, market-based policy implementation, and mitigation action recognition. Instead, we must realize that our desired future calls for the development and use of multiple corporate GHG accounting metrics—in a multi-statement reporting framework—where each metric conveys distinct types of information intentionally designed to support specific intended uses (Figure 1).

2.) A corporate “value chain” is a practical framework for establishing GHG inventory boundaries (i.e., assigning individual organizations responsibility for “their” GHG emissions). In contrast, we should recognize that our desired future requires a less ambiguous corporate accountability framework and approach to inventory boundary-setting. This new approach to GHG accounting boundaries needs to achieve an appropriate degree of sensitivity to measure actual changes in emissions over time and some degree of comparability2 across companies in keeping with the intended use of the GHG metric. For the intended use of voluntary corporate target setting and leadership recognition, the corporate GHG boundary setting rules should be drawn to maximize the efficacy of the recognition program (i.e., aggregate depth and breadth of participation and mitigation action), which will likely mean narrower boundaries for indirect emissions and removals. Maximizing mitigation action in a voluntary reporting context is the ultimate goal, not maximizing, for its own sake, the scope of value chain responsibility that each company is pushed to accept.3

3.) Ideal corporate climate leadership is demonstrated by the achievement of “corporate net zero,” whereby a corporation claims to no longer be contributing to global warming. Corporate net zero, as it has been established, must necessarily also incorporate mechanisms allowing companies to compensate for all the “residual” emissions they are unable to abate (e.g., offsetting using carbon credits or other emission attribute certificates). Instead of corporate net zero with compensation, the path to our desired future demands that we reframe corporate leadership as a combination of an accountability target for emissions unambiguously allocated to a company (i.e., a physical GHG inventory reduction target) and a separately tracked “beyond inventory mitigation” goal. By making compensation mechanisms a core aspect of the accountability framework for corporate climate leadership, the existing paradigm has created a moral defect in the eyes of stakeholders—companies see no other option than to use attribute certificates or carbon credits to compensate for an impractically expansive emissions accountability framework. The combination of a reduction target with clear accountability and a separate mitigation intervention goal would:

→ Recognize companies for reducing their inventoried emissions—aligned with science-based targets—from sources for which they have been assigned clear and more exclusive responsibility, and

→ Reward achievement of contribution goals toward global net zero by companies making ambitious mitigation interventions that advance science-aligned mitigation in their “beyond inventory” value chains, as well as outside their value chain.

A compensation to contribution reframing eliminates the perception that companies can be absolved of responsibility through offsetting, while appropriately accounting for and recognizing both internal and external climate actions taken by companies through separate GHG statements. For a deeper dive on the moral dilemma and technical issues with this framing of corporate net zero as “compensation,” please read this article.

4.) Corporate GHG inventories should be structured to account for all the products—goods and services—a company produces, purchases, and sells. In other words, the foundational unit of a corporate inventory is the product, and a meaningful inventory is constructed through the aggregation of numerous product-level life cycle assessments (LCAs). By contrast, the conventional definition of a GHG inventory involves identifying physical sources and sinks—not product flows—within a clearly defined accounting boundary, and quantifying emissions and removals from those physical sources and sinks, respectively. The challenge that arises under the current Scope 3 approach to accounting for indirect emissions is that it is rare for physical sources or sinks to be identified.4 This raises the question: should reports that include Scope 3 emissions, as elaborated in the GHG Protocol, even be referred to as GHG inventories? Read installments number N-1, N-5, and N-6 for a deeper dive on the problems with the current Scope 3 approach. At the very least, Scope 3 does not qualify as a physical GHG inventory method because it does not identify what sources and sinks are included. How can companies mitigate and then account for and report on emission impacts to specific emission sources they have not identified?5

The role of market-based approaches, including renewable energy attribute claims, in a multi-statement approach to corporate GHG accounting is specifically elaborated on in the companion N.7 bis installment of this series.

Hard truths

Can we all finally admit it? As currently structured, Scope 3 does not work as needed. There are reasonable justifications for asking corporations to account for and report “indirect emissions” occurring from sources beyond their organizational (Scope 1) boundaries. Yet, as I have discussed here and here, the LCA approach to setting corporate GHG accounting boundaries for indirect emissions in the GHG Protocol and ISO 14064-1 is fundamentally flawed. To put it simply, it is a mass delusion that we can perform an LCA on an entire company in a manner that will produce a meaningful time series of emission estimates against which to judge the achievement of corporate emission reduction targets and overall GHG performance. I justify this conclusion with the following:

The underlying driver of voluntary corporate climate action is to be recognized for leadership in addressing GHG emissions and removals. That recognition is dependent on a credible accountability framework using quantitative corporate GHG metrics. However, the current accounting boundary setting rules under Scope 3 are overly expansive, ambiguous, massively overlapping, and looping.6 Value chains are too extensive to be the basis for quantitatively defining accountability, and they result in an indeterminate number of companies being asked to take responsibility for the same unit of emissions. Scope 3 establishes what is effectively an opaque accountability framework. The outcome is that no company can realistically eliminate “its” Scope 3 emissions until most other companies do as well. Functionally, this is a system of excessively collective responsibility.7 Yet, social science generally finds that more exclusive (i.e., individual) accountability mechanisms drive behavioral changes in organizations better than expansive approaches to accountability.8 Further, corporate GHG mitigation action largely exists in a voluntary context where actions are driven by a limited number of leading companies that seek stakeholder recognition,9 while most companies do not participate.10 For a company to realistically eliminate its Scope 3 emissions, it would need to have special powers to coerce widespread participation across a competitive global economy—an economy with regulations that are often aimed at minimizing the market power of individual companies. So, is it practical to expect these few leading companies to reduce the emissions from all companies somehow connected to their value chains?

The current Scope 3 paradigm produces corporate inventory totals and trends in those totals that are not meaningful measures of individual company performance or changes in that performance.11 Instead, Scope 3 is primarily year-to-year sensitive only to how much a company spends or sells within broad product and service categories, and not to the effects of corporate mitigation actions. So, companies find that they are only able to show substantial overall reductions in their indirect emissions by spending or selling less. And yet, most emission totals reported by companies are currently dominated by Scope 3 estimates (though this size comparison between Scopes is misleading). Scope 3, for most companies, is primarily estimated using crude spend-based or product consumption-based data that does not involve the identification of specific physical emission sources. As a result, these estimates are typically not representative of each company’s actual value chain (i.e., average emission factors are often used for broad product classes rather than factors specific to a company’s consumption or production, and these factors are also often out of date and do not adjust to real-world value chain dynamics).

As far as we have been able to identify, no company has conducted a thorough mapping of the physically emitting processes in its “full” value chain.12 Therefore, companies do not know what specific emission sources are in their imagined value chains, nor do they know what emissions or emission sources they are being told to take responsibility for reducing under Scope 3. Given that the physical sources remain unidentified, it is not possible for companies to meaningfully quantify how much these sources are emitting. Further, it is not possible to apply the GHG Protocol’s principle of completeness to assess whether a company has reported “all” value chain emissions.13 Finally, spend-based Scope 3 emission estimates also generally lack the process resolution needed to identify particular “hot spots” of large emission sources for subsequent mitigation option identification and interventions.

Have climate leader companies been set up to fail?

The current paradigm of Scope 3 GHG accounting puts companies in a situation in which they have no realistic means of achieving their “science-aligned” targets through their own internal mitigation efforts. We have created this situation by treating it as an article of faith that the proper way to recognize and assign responsibility to a company for reducing GHG emissions (i.e., defining what “their emissions” means) is to do so based on value chain LCA thinking. But there are good theoretical and practical reasons why this faith is misplaced. To state it another way, we can clearly define what net-zero emissions mean on a global scale; but, on a corporate or other sub-global scale, how we allocate responsibility for emissions—and therefore define corporate net zero— is a normative choice about how we should allocate the scope of responsibility for emission sources to individual companies. There is no technically correct answer to this dilemma. We can and should change these normative emission allocation choices and transform them into a meaningful and effective GHG accounting framework.

The current approach to corporate reporting and target setting is also based upon a flawed theory of change. This theory implicitly assumes that maximizing the scope and collectivization of emissions that companies are assigned responsibility for will maximize corporate climate action and aggregate emission reductions. Yet, the actual result is to dilute and obscure responsibility and to frustrate corporate action and the recognition that largely drives it. In the context of corporate target setting, we should instead allocate responsibility for emissions to companies in a manner that maximizes the impact of internal corporate GHG mitigation activities, which is a function of how much each company does and how many companies take action.

This maximization can be better achieved by designing GHG inventory boundaries, for both direct and select indirect emissions, in a manner that supports accountability, which means designing for unambiguous, more exclusive assignment of responsibility at the physical source and sink level. By doing so, we will also foster better accuracy, time series consistency, and metric sensitivity in GHG reporting. Target-setting programs and the companies that participate in them are currently frustrated by the expansive paradigm of assigning responsibility. Although effective accountability can and should include assigning responsibility for selected indirect emissions (e.g., downstream fuel combustion emissions from oil companies), this selection must be done with intention for each industry (see Installment N.6).

Those who see this as too much change for companies and non-profit GHG programs to handle, especially when we are under time pressure to act, should consider the experience of companies that do try to take action within the existing Scope 3 framework. When companies take actions to mitigate emissions from sources within or in the vicinity of their value chain, they expect that these changes will be reflected in their Scope 3 estimates over time. Yet, they are frustrated when they realize that Scope 3 estimates are methodologically insensitive to the physical changes they have worked with suppliers to make (because of the use of spend- or consumption-based estimation approaches).

It is no surprise then that under the current corporate GHG reporting and target-setting frameworks, companies turn to market-based claims such as carbon credits, renewable energy certificates (RECs), and other environmental attribute certificates (EACs) to attempt to meet targets that ask them to reduce indirect emissions from sources that they are not even able to identify. And then, when companies make compensation claims based on EACs, they are criticized for greenwashing and not “taking responsibility for their emissions.”14

I believe we will remain trapped in this doom loop—frustrating and then criticizing the few companies attempting to lead on climate—so long as our GHG accounting and target-setting frameworks are grounded in this paradigm. So long as we continue attempting to extend corporate GHG emissions accountability across unbounded value chains, and LCA is relied upon to quantify indirect emissions, this loop will exist. I do not believe this cycle can be broken by introducing new market-based GHG inventory approaches or EAC markets, as they distract from the foundational issues. Instead, we must address the root causes of the problem to move toward a future where corporate action is respected because it has environmental integrity and moral clarity.

A solution

As I discussed in a past installment, there are a number of intended uses for corporate GHG metrics. And no single metric, such as a corporate GHG inventory, can meaningfully serve all uses. By attempting to, the current GHG Protocol corporate standard is ineffective at meeting the needs of all purposes of GHG accounting. Therefore, a key part of the solution to the problems discussed above is transitioning to a multi-statement corporate reporting framework that employs multiple GHG and GHG-related metrics.

The proposed multi-statement framework in Figure 1 focuses on the intended use of measuring corporate GHG performance against internal GHG reduction targets and broader mitigation contribution goals. In terms of GHG accounting, this intended use can be further broken down as: i) tracking a company’s GHG emissions performance over time, and ii) comparing relative corporate GHG performance across companies. The allocational GHG accounting metric in Figure 1 supports this use for a company’s internal (i.e., inventoried) emissions, while the consequential GHG accounting metric supports it for companies’ “beyond inventory” mitigation actions. For some industries, non-GHG transition indicators provide simpler performance measures that supplement these other two metrics.

The consequential metric also supports the use of market mechanisms by quantitatively evaluating and reporting the efficacy of actions taken through these mechanisms, as well as other corporate mitigation investments and interventions. The value chain analysis then serves the purpose of informing companies where to look for potential high-impact mitigation options.

With an explicit focus on fostering comparability between reporting across companies, this multi-statement framework also supports investors and financial regulators with their intended use of comparing companies’ GHG performance. However, the framework does not support the intended use of measuring companies’ climate risk exposure, as this is not a GHG accounting question. The framework also does not evaluate the relative GHG performance of different products and services, as this is a product-level, not a corporate-level, GHG accounting question.

Figure 1. Illustration of proposed multi-statement corporate GHG reporting15

Each of the four statements in this proposed framework is described further below:

The first statement—a Physical Inventory statement—modifies existing corporate GHG inventorying standards under the GHG Protocol and ISO 14064-1. This Physical Inventory statement allocates responsibility for emissions to individual companies (i.e., applies an allocational GHG accounting method).16 The main differences with the current GHG Protocol corporate standard are that this Physical Inventory statement: i) applies clear accounting boundaries based on intentionally selected sources and sinks, and ii) does not incorporate market-based approaches to estimating Scope 2 or other emissions. These select sources and sinks must be physically identified17 and distinctively quantified, thereby producing time series emission estimates that are a meaningfully sensitive measure of corporate GHG performance—including internal mitigation actions. It is also possible to design GHG accounting boundaries to achieve acceptable comparability across companies in the same industry.18 Companies can set science-aligned targets for reducing “their emissions” using this metric because it provides a clear line of sight to all emission sources for which they are allocated responsibility. Lastly, this statement should exclude any adjustments to the estimates for the purpose of compensating for emissions (e.g., offsetting) or other claims through EACs or other market-based claims. Instead, EACs, as well as other market-based interventions, are accounted for under the second statement. Financial activities, such as those referenced in the Scope 3 category 15, are also treated as interventions and not reported as part of a GHG inventory.

The second statement—a Mitigation Intervention statement—is a new type of corporate GHG reporting metric that accounts for the aggregate impacts of corporate interventions, which are estimated utilizing consequential GHG accounting methods. This statement provides a standard for companies to report on the avoided emissions and enhanced removals resulting from “recognized ambitious” interventions. It also supports the aggregation of impacts across interventions and, with this, the setting of aggregate corporate contribution goals to global mitigation. Only the effects of interventions on sources and sinks outside the intervening company’s Physical Inventory boundaries or in activity pools are to be reported in the Mitigation Intervention statement (i.e., “beyond inventory mitigation”). These sources and sinks, however, may still be viewed as being within a company’s value chain.19

The third statement—Non-GHG Transition Indicators—is bespoke to each industry. For some industries, there are established global net-zero emissions transition pathways that involve specific technological changes (e.g., transition from manufacturing of internal combustion vehicles to electric vehicles for the automotive industry). For industries where widely accepted transition indicators can be specified, companies and target-setting programs can quantitatively track these indicators to supplement the GHG metrics in the previous two statements.20 For some industries, it may not be practical to construct standardized transition indicators.

The fourth statement—a Value Chain Analysis—largely replicates what is currently reported under the existing Scope 3 standard using spend-based methods. It provides an expansive, albeit poorly resolved and highly uncertain, view of emissions associated with a wide range of activities that LCA models predict are associated with spending on or sales of broad categories of products and services by a company. The resulting information can be instructive for identifying products in a company’s value chain that are likely to involve highly emitting upstream or downstream processes, which should be prioritized for investigation and identification of mitigation options. The ex-post impacts of any implemented options taken to mitigate “beyond inventory” emission sources in these processes would then need to be quantified and reported under the Mitigation Intervention statement. Given that emission estimates produced with value chain analysis are largely insensitive to year-to-year changes in a company’s real-world value chain, it is unnecessary to prepare it annually; instead, companies should only update it after major structural changes occur in their supplier relationships or product design.

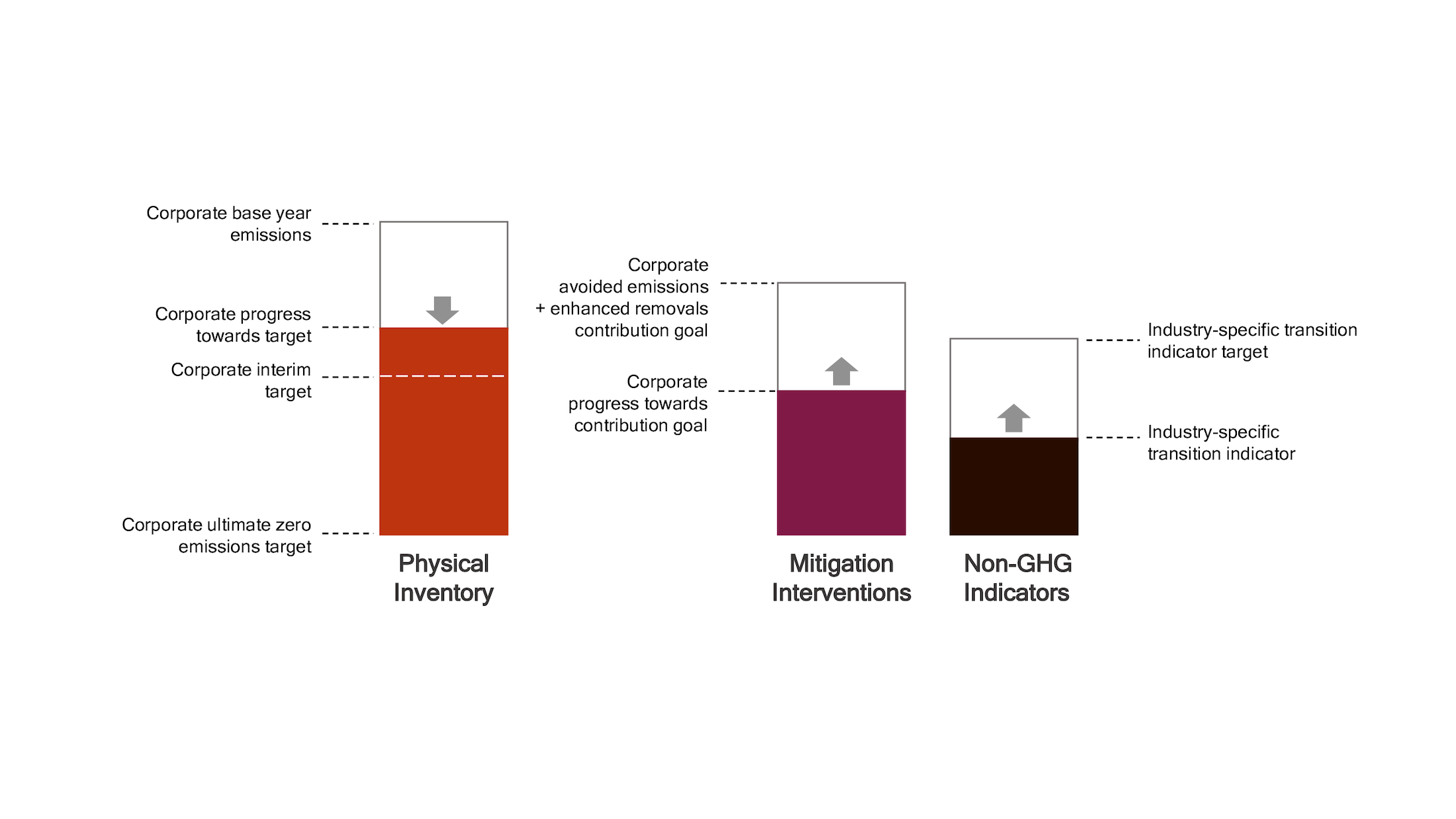

This kind of multi-statement reporting framework will better support corporate leadership recognition programs, such as the Science-Based Targets Initiative (SBTi), by providing multiple “unmuddled” corporate performance metrics to use (Figure 2). A Physical Inventory statement supports the tracking of corporate reduction targets aligned to global net-zero sector pathways that companies can both conduct concrete mitigation planning for and then be held accountable to. A Mitigation Intervention statement to track progress toward corporate cumulative avoided emissions and enhanced removal contribution goals established by recognition programs.21 And for industries with known technological transition pathways, targets for industry-specific indicators can be set to track individual companies’ progress.22 Recognition programs may also choose to combine and weight metrics from different statements into an overall corporate performance score.

Figure 2. Illustration of multi-statement progress tracking with annual corporate inventory target, annual contribution goal, and annual sector-specific non-GHG transition indicator target23

This combination of reporting statements would eliminate the problems discussed above. For example, the combination resolves the complex problems introduced by market-based approaches to Scope 1, 2, and 3 reporting. Financial interventions taken by companies for the purpose of GHG mitigation that are conducted and amassed through EAC markets are reported as estimates of the intervention’s avoided emissions and enhanced removal impacts, in place of flawed consumption matching claims in their corporate GHG inventory. The next installment in this series addresses in depth how the problems with market-based approaches are resolved with this multi-statement framework (see Installment N.7 bis).

This combination also eliminates the need to solve intractable value chain of custody and traceability problems, since these interventions would no longer be shoved into the corporate GHG inventory as awkward adjustments that result in a departure from physical GHG inventory good practice (i.e., allocating emissions based on purely financial connections and blending consequential and allocational methods). For corporate GHG inventories, resources should not be expended attempting to address chain of custody and traceability, double counting, and residual and other emission factor adjustment problems for Scopes 2, and especially Scope 3. These efforts are largely unproductive and unnecessary distractions.24 With a multi-statement framework, corporate resources can instead be directed to separate “intra-inventory” and “beyond inventory” mitigation actions that are transparently accounted for and recognized using different metrics. Because the Physical Inventory statement is not treated as a massive multi-product collection of LCAs, there is no product chain of custody or traceability ambiguity, as its boundaries are based upon clearly identified emission sources and sinks.

Again, under the Mitigation Intervention statement, the sources and sinks affected by a company’s interventions are only recognized for reporting if they are outside their clearly visible Physical Inventory boundaries or in activity pools. As a result, there is no double-counting of the effects of mitigation actions taken by a given company between the two statements.25

Concluding thoughts

The current corporate GHG accounting paradigm, dominated by extremely uncertain and expansive Scope 3 accounting boundaries and based on life cycle assessment thinking, has created reporting and recognition systems that frustrate meaningful corporate climate action. By primarily or solely relying on value chain emissions as the all-encompassing metric for corporate accountability, we have inadvertently constructed what amounts to an excessively collective responsibility framework that dilutes individual corporate accountability and obscures recognition of the very mitigation actions we seek to encourage. Some joint responsibility between clearly identified value chain partners can be managed in a GHG accountability framework, and the proposed intentional approach to allocating indirect emissions for each industry can facilitate, rather than frustrate, coordinated action between connected companies.

The spend-based estimates that are the dominant basis of Scope 3 reporting are insensitive to most corporate mitigation efforts, creating a disconnect between action and recognition that undermines the voluntary nature of corporate climate leadership. Meanwhile, the predictable turn to market-based approaches and offsetting mechanisms to meet otherwise unworkable targets through compensation claims has spawned legitimate greenwashing and morality concerns.

The multi-statement reporting framework outlined here offers a fundamentally different approach—one that recognizes that no single metric can serve the different purposes for which corporate GHG metrics are used. This paradigm shift requires abandoning flawed legacy assumptions about corporate climate responsibility. It means accepting that how we allocate emissions responsibility to companies requires unambiguous boundaries around identifiable physical sources, not expansive “full corporate value chain” GHG accounting fantasies.

The transition to multi-statement corporate reporting will not be without challenges. It will require developing industry-specific boundary-setting rules, establishing credible consequential accounting methodologies for recognized types of interventions (a new report on this topic is forthcoming), and then adapting existing target-setting and recognition programs (see Table 1). However, these challenges pale in comparison to the dysfunction of our current corporate GHG accounting framework. We should not wait to fix our GHG accounting protocols and standards, and let fear of upsetting the status quo block us from the path to our desired future.

The stakes are high. Climate change demands rapid, large-scale GHG mitigation that can only be achieved with corporate participation and action. Our current GHG accounting paradigm is impeding such action by creating unrealistic expectations, obscuring meaningful progress, and generating cynicism about corporate climate commitments.

The choice before us is simple: continue down the current path of incremental refinements to a fundamentally flawed GHG accounting framework, or embrace the transformative change needed to generate corporate GHG accounting results that meaningfully capture the realities of how businesses operate and climate action occurs. The future of corporate climate action likely depends on making the right choice and not being afraid of change.

Table 1. Summary comparison of the current GHG Protocol corporate standard and proposed multi-statement framework

GHG Metrics

Current GHG Protocol Corporate Inventory Standard

Multi-statement Framework

GHG inventory

• Scope 1

• Scope 2

• Scope 3

✔️

Both location and market-based required, with latter based on MWh matching with unevaluated impacts

Based on expansive and ambiguous value chain boundaries and spend-based life-cycle assessment methods

✔️

Only location-based

Included with narrower and clearly delimited accounting boundaries, estimates based on physical estimation methods for direct and indirect emission sources

Market-based inventory statement

Not a separate statement (but being considered in update), instead included in GHG inventory for Scope 2 and proposed for Scopes 1 & 3

Not a separate statement, impacts of market-based instruments accounted for under consequential impact metric

Consequential impact metric

✗

No metric or reporting framework provided, generic project guidance available

✔️

Mitigation Intervention statement

Non-GHG transition indicators

✗

Not addressed

✔️

For applicable industries and activities

Value chain analysis

Included in GHG inventory as Scope 3

✔️

Value Chain Analysis serves same function as current Scope 3, but reported as a separate statement

I am thankful for the insightful comments and discussions with Tani Colbert-Sangree (GHGMI), Mark Trexler (The Climatographers), Alissa Benchimol (GHGMI), Erika Barnett (GHGMI), Matthew Brander (University of Edinburgh), and Derik Broekhoff (SEI).

Recommended Citation

Gillenwater, M., (2025). What is Greenhouse Gas Accounting? Paradigm shift to multi-statement GHG reporting. Seattle, WA. Greenhouse Gas Management Institute, August 2025. https://ghginstitute.org/2025/09/03/multi-statement-ghg-reporting/

Although I will frequently refer only to GHG emissions for the sake of brevity, the reader should interpret this to implicitly include emissions and removals.

What makes entities comparable? Entities are comparable if they share a core set of common properties, which then allows for analysis and highlighting of differences across other selected properties. If two entities belong to entirely different categories that lack any major shared properties, they are not comparable. But comparability does not mean that all aspects of two companies must be the same, only that the range of differences is sufficiently limited to give meaning to the differences present in the compared metric.

It is unhelpful for corporate GHG inventory and target-setting standards to impose thresholds for permissible exclusions of indirect emissions without providing a clear and unambiguous definition of “complete.” For example, for target reporting or target setting purposes, permitting companies to exclude 5% of a highly subjective and easy-to-manipulate total emissions value is not an effective basis for standardization.

There is a misleading nomenclature problem embedded in the GHG Protocol in that it uses the term “activity data” in two distinct manners. The established definition of activity data for GHG inventories is that it is a variable measuring an output or input from a process that physically emits or removes GHGs. This definition is used by the IPCC and by the GHG Protocol in the context of Scope 1. Yet, with Scope 3, activity data refers to financial data or outputs and inputs that are indirectly associated with a wide number of emitting and removing processes, which are generally unspecified (e.g., purchasing office equipment). An “activity” such as buying a product (e.g., a toaster) is not a technically sufficient basis for defining the GHG inventory boundary. Instead, to specify a GHG accounting boundary, one must clearly identify physical emission sources and sinks.

Companies should still be encouraged to purchase, design, and sell products with lower GHG impacts; however, recognition for such decisions is not best recognized through a GHG inventory metric.

Accounting boundaries are looping when one company’s upstream suppliers are also their downstream customers, which is surprisingly common.

Imagine being a student and learning that to join a prestigious school, you would be held accountable for the grades of all the students in that school. Or the grades of all the students in all the schools in the city. Sounds a bit impractical? In effect, this is what Scope 3 does for companies in the context of voluntary corporate GHG reporting and recognition. Alternatively, the school uses group-based learning where modest-sized groups of students work together on a range of projects. Within each group, the students know each other well. My proposal is that we shift our GHG accountability framework for corporate indirect emissions to something that looks more like the student group scale than the all the students in the city scale.

See Hardin (1968); Feeny, et al. (1990); and Ostrom (1990). More generally, research appears to better support the efficacy of shaming approaches for changing corporate environmental behavior compared to a leadership recognition approach (Chatterji et al., 2009). For example, the U.S. Environmental Protection Agency’s Toxics Release Inventory (TRI) has been well studied and associated with significant reductions in environmental emissions, as companies seek to avoid negative publicity.

Stakeholders include investors, customers, the broader public, and especially employees.

Despite what many believe, the collectivization of responsibility in the context of voluntary corporate climate recognition and action is a “bug,” not a “feature” of the current approach to Scope 3.

Further complicating the interpretation of emission time series trends is that Scope 3 inventory accounting boundaries are a temporal mash-up of emissions occurring in the past, current, and future. Across various Scope 3 categories, it mixes annual and lifetime (or life cycle stage) cumulative emissions into one aggregate total reported as if it occurs in a single year. For example, emissions from the use of sold products are often totaled over the product’s lifetime. But employee commuting emissions are reported for the year in which they occur.

If you know of such a unicorn of a company, please contact us! info@GHGinstitute.org

In fact, the GHG Protocol Scope 3 standard acknowledges that “completeness” is likely infeasible: “Companies should strive for completeness in mapping the value chain, but it is acknowledged that achieving 100 percent completeness may not be feasible. Companies may establish their own policy for mapping the value chain, which may include creating representative, rather than exhaustive, lists of purchased products, sold products, suppliers, and other value chain partners.” (section 6.1, page 59)

Theoretically, one could argue that there is no “beyond value chain mitigation,” because when a company invests in a mitigation activity (e.g., through a direct investment or EAC purchase), that investment becomes part of their Scope 3 Category 15.

I am grateful for the contributions of Gilles Dufrasne, Jonathan Crook, Injy Johnstone, Thomas Day, and Derik Broekhoff in developing earlier iterations of this multi-statement framework.

It may also be applied to individual corporate business lines/units in cases where companies are diversified across multiple industries, or to a collection of corporate entities if an industrial process has been disaggregated across these entities.

These sources and sinks may change over time as the assets and processes of the company change.

Although a goal of this new GHG inventory boundary setting reform is to foster comparability across companies in an industry, I would argue that it still makes sense for intended uses of a corporate GHG metric that do not call for comparability across companies, as it addresses the problems of accountability, quantifiability, and actionability that companies and target setting programs face with the current approach to Scope 3 indirect emissions.

Because of the ambiguous boundaries of value chains and Scope 3, the concept of “beyond value chain mitigation” has no useful applied meaning. Whether an emission source is beyond the value chain of a given company is a subjective determination with large variability.

We will be providing suggestions for setting these corporate contribution goals in a future installment.

These sorts of transition indicators are already being incorporated into some draft SBTi sectoral standards.

Removals and enhanced removals are not presented for simplicity of presentation.

Chain of custody and traceability questions can still be relevant for the purpose of product-level attribute claims for product labeling, which is a fundamentally different purpose than reporting, over time, GHG emissions and removals allocated to an entire company (i.e., a corporate GHG inventory).

Interventions within GHG accounting activity pools, such as electricity consumption, could be reflected in both the Physical Inventory and Mitigation Intervention statements. For example, some portion of the impact of a corporate intervention in the electric power sector reported under the Mitigation Intervention statement could also have a small effect on the grid average emission factor used in the same company’s Scope 2 indirect emissions reporting. We deem these minor cases of dual impact reporting across two separate statements an inherent artifact of activity pools that does not inhibit the use of each statement for appropriate intended uses because targets/goals are applied to each statement separately.

Hello Michael. I have been very interested in reading your thoughts across all the What is GHG accounting installments. These last ones were very insightful as to fleshing out a solution to the various issues described in previous entries. Noticing that you reply to some of these comments, I wanted to ask a few questions.

First of all, a physical inventory statement with specified boundaries for different sectors (and no double counting!) makes sense to me, and I understand that this is a conceptual proposal for now, but I am wondering as to the practical issues that this could entail, for example: could this leave some companies, (whose physical emissions are “covered” in one of their clients’ boundaries) without any physical emissions to report? What about heavy emitters who participate in various sectors? And what if these boundaries overlap between downstream companies? You acknowledge that these issues would remain open and they may be preferable to the status quo that (you have convinced me) is a mess, still, these questions bother me and I wonder if you have thought of some possible solutions, or if I’m getting something wrong.

Furthermore, I am keen to ask you what your advice would be for GHG practitioners that have really no choice but to work with the current amalgam of GHG Protocol, ISO and SBTi standards that do not provide a multi-statement, fit-for-purpose way of reporting emissions. Other than involving ourselves in these standards’ revision processes and advocating for better GHG accounting, when it comes to actual accounting right now, what are some good practices or how can we best work under the standards’ current guidance, recognizing and being aware that the fundamental issues that you have thus far described, will not be solved overnight.

These are great questions, and I love to see you and others engaging with these concepts.

First, I do not see the implementation of the Physical Inventory statement leaving any company with nothing to report. Additivity (i.e., no double counting) is intentionally applied only across companies within the same industry that share common accounting boundary setting rules. And every company will still have a combination of direct and indirect emissions in their boundary (although what portion is direct vs indirect may vary across companies based on how outsourced vs. vertically integrated they are). Please refer to Installments N.5 and 6, which go through the allocation boundary concept here. Installment N.3 might also provide useful background on allocation and additivity concepts, where I refer generically to an industry as a “population of companies”. I apologize that the points are spread across so many different essays and that I don’t do a better job explaining them. It is a lot to try to explain when you are building up from fundamentals.

To your question, it is fine that there is overlap between an upstream and a downstream company. The Physical Inventory statement allows this. The purpose of being more intentional on the boundaries is not to eliminate any overlap between the inventory of any company in any industry. But, instead to do three things: 1) to foster comparability in inventories between companies doing basically the same thing (i.e., in the same industry); 2) make the inventory boundaries for a company visible to the company so that sources can be quantified with meaningful sensitivity; and 3) and avoid overlap between companies in the same industry (versus companies in other industries).

And for companies that do a variety of things (i.e., engage in multiple industries), then it would make far more sense to break down their inventory by business unit/industry segment so that like can be compared with like, and targets can be set for each different kind of corporate activity separately. Obviously, we need to move to more sectoral detail, which is what SBTi has already been doing. Our inventories are inhibiting this maturation currently, when they should be leading it.

To your question about what to do now, given the status quo, I wish I had something magical to offer. Because the status quo is a mess and too many are in denial, or at least stuck thinking that the way of the past is the only way we can think and do things. Having said that, I tell companies and consultants to be the change they want to see in the world. If you want to make interventions, then draft up your own impact analysis using consequential methods and report that separately as avoided emissions. And write something about how you think there needs to be a recognized reporting and contribution goal-setting framework for that kind of information. Companies have a lot of flexibility in what they report, so if the standards are not keeping up with the needs, then get ahead of them. In other words, innovate a bit rather than waiting for the standards to innovate, because they are quite change-adverse. And, yes, also get engaged in the standard setting processes.

For me, the reason companies might want to use market-based instruments to address their Scope 3 is because they don’t have a good alternative way to take action. Usually because of traceability and also because of shared supply chains (which means risking sharing their investment benefits with freeloaders). To fix this in my view, rather than changing fundamentals of accounting is that an organisation doesn’t have the same level of responsibility or ability to act on all parts of its value chain – there are many others with associated responsibility that can be harnessed. Ignoring these “hard to reach” parts as I think you’re suggesting will likely just mean no-one tackles them. Which also sounds like an alternative green-washing risk – “this bit was too hard, so you ignored it”.

Well, the purpose of creating additional statements more fit to purpose is to create that alternative. And I think you mean they don’t have a good alternative to get recognized for the impacts of actions. I think I address all these concerns in the companion installment 7bis on market-based approaches. As to the inventory boundaries, I find it a bit of a fantasy that an voluntary accountability and target setting scheme can work when responsibility is set up in such an ambiguous and imaginary manner. No company has ever mapped all the sources and sinks in their Scope 3 value chain, as far as we have been able to determine. If you or anyone has an example to share, please do so. Ultimately, we are talking about GHG accounting that needs to produce metrics that measure something useful. Wishing that we had a metric that measures someone doesn’t make it true. There are limits to what we can effectively achieve with a voluntary corporate accountability scheme. Ignoring those limits only makes the scheme more ineffective.

Comments